njhowie

Thinks s/he gets paid by the post

- Joined

- Mar 11, 2012

- Messages

- 3,931

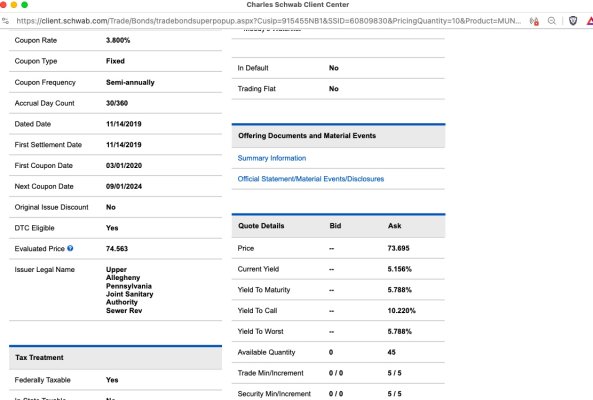

Based on what I'm seeing as far as pricing weakness in the housing/mortgage munis, there seems to be an expectation that there will be a wave of redemptions coming. The munis, many recently issued, have call dates a fair ways off into the future. However, they may be looking to invoke their extraordinary redemption/prepayment clauses to redeem at will.

I just nibbled on a taxable Colorado AAA 2053 maturity, 2032 call, 6.25% coupon, recently issued in September. I paid 102.5. I figure the premium isn't much at this price. If they call in under 5 months I'll lose a few dollars. If not, looks like a great buy.

I just nibbled on a taxable Colorado AAA 2053 maturity, 2032 call, 6.25% coupon, recently issued in September. I paid 102.5. I figure the premium isn't much at this price. If they call in under 5 months I'll lose a few dollars. If not, looks like a great buy.