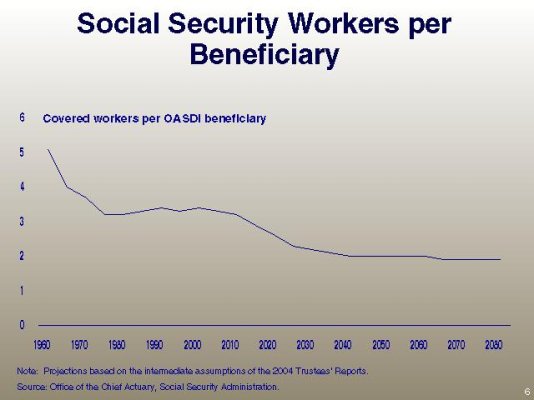

Once SS begins having a cash-flow deficit (which happened for the first time in 2010), here are the choices the U.S. Government (USG) will face to remedy the shortfall. I have created 5 general categories.

(1) The USG can authorize an increase in SS Payroll taxes to close the deficit. This can be done by raising the income cap, the tax rate, or both. The SSA will then not have to begin redeeming its special Social Security Trust Fund (SSTF) bonds.

(2) The USG can authorize a reduction of SS benefits to close the deficit. This can be done as an across-the-board cut, some form of price-indexing, a reduction in the benefit formula (i.e. bend points), raising the retirement age, or anything other benefit reduction method I have not mentioned or thought of.

(3) If neither Option (1) nor Option (2) is chosen, or the amount of SS deficit reduction achieved by them is not enough to cover the entire shortfall, then the special SSTF bonds will have to begin getting redeemed. This will transfer the (remaining) SS deficit from SS to the rest of the USG. What will the USG do then? It can raise non-payroll taxes, probably mostly income taxes because they are the largest revenue source.

(4) The USG can reduce (discretionary) spending outside of SS. This includes everything else in the federal budget other than interest on the national debt (because the USG is not going to default on its existing bonds).

(5) The USG can borrow from those outside the USG by issuing new bonds to generate the cash needed to pay off the SSTF bonds. This is basically borrowing from Peter to pay Paul. This is probably the easiest to be done politically, as long as we continue to have buyers for these new bonds. This new debt will be on top of the existing debt and any new debt generated by the rest of the current federal budget.

If, by some huge miracle, the rest of the federal budget is in a surplus, that surplus can be used to pay off some or all of the SSTF’s bonds as they are redeemed. Of course, those surplus dollars will not be able to be used to retire any non-SS debt or be spent on other things or used for tax cuts. These are more tough choices for the Congress and the President, of course.

Under the current “Do-Nothing Plan,” we will probably end up with Option (5), as we did in 2010. However, the details of these options is where the tough choices will be made.

Now, let us advance to the later date of legal insolvency, the one those on the Left love to quote – around 2037, give or take a few years. What will be the choices we face when the cashless SSTF’s bonds are completely redeemed?

(1) The USG can authorize an increase in SS Payroll taxes to close the deficit. This can be done by raising the income cap or the tax rate, or both.

(2) The USG can authorize a reduction of SS benefits to close the deficit. This can be done as an across-the-board cut, some form of price-indexing, a reduction in the benefit formula (i.e. bend points), raising the retirement age, or anything other benefit reduction method I have not mentioned or thought of.

(3) If neither option (1) or (2) is chosen, or the amount of SS deficit reduction achieved by them is not enough to cover the entire shortfall, then there will be have to be an infusion of cash from the rest of the USG to cover the SS deficit. What will the USG do then? It can raise non-payroll taxes, probably income taxes because they are the largest revenue source.

(4) The USG can reduce (discretionary) spending outside of SS. This includes everything else in the federal budget other than interest on the national debt (because the USG is not going to default on its existing bonds).

(5) The USG can borrow from those outside the USG by issuing new bonds to generate the cash needed to cover the SS deficit. This is probably the easiest to be done politically, as long as we continue to have buyers for these new bonds. This new debt will be on top of the existing debt and any new debt generated by the rest of the current federal budget.

If, by some huge miracle, the rest of the federal budget is in a surplus, that surplus can be used to cover some or all of the SS deficit. Of course, those surplus dollars will not be able to be used to retire any non-SS debt or be spent on other things or used for tax cuts. These are more tough choices for the Congress and the President, of course.

Under the current “Do-Nothing Plan,” we will probably end up with Option (2) - as that is what current law requires – that SS benefits be paid only using what funds are available after the cashless SSTF is exhausted. Will the USG enact any of the options to lessen the overall effects of Option (2)? I don’t know.

The point of this exercise is to show that once SS goes into a cash-flow deficit, the choices the USG has to close that deficit are basically the same before or after the SSTF’s bonds are completely exhausted.