gwix98

Recycles dryer sheets

Anyone using preferreds for income? Especially ETF’s or conventional funds?

What do you mean by "income"? Standard equity ETFs/funds provide income as well. Perhaps some of it is from growth rather than dividends, but that isn't a useful distinction. Well, it might be useful in some cases, the growth might have some tax advantages/flexibility for you.

-ERD50

Earlier in 2019, I bought a number of individual preferreds.... have already had 4 called... currently have 19 issues that have a weighted-average yield of about 5.75% and yields ranging from 5.05% to 7.30%.... most are BBB or BBB-, with a couple BBs.... names like Wells Fargo, JPM Chase, MetLife, The Hartford, Duke Energy, etc. and some lesser recognizable names. Its about 10% of my nestegg and I view it as part of my fixed income allocation. The issues have appreciated handsomely since I bought them and my YTD return has been about 9.25%... so I'm pretty happy with the results.

Come on in, the water is fine.

VWEHX Vanguard High Yield Bond) which is a little higher quality junk bond fund has returned over 13% this year with a 5.0% yield. I'm curious why a person reaching for yield wouldn't just buy this fund. I do not own preferred stocks or high yield bond funds. I am very unfamiliar with preferred stock, so my question is genuine.

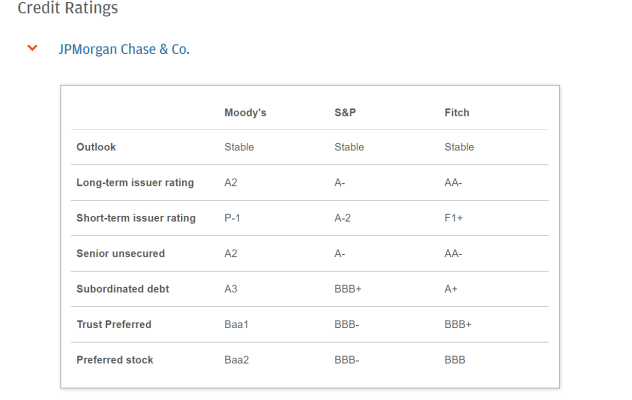

For one, I think you are misinterpreting the credit quality ratings... the fact that I provided S&P ratings and the VWEHX credit quality table is in Moody's ratings is most of the problem.

Most of my preferreds are S&P BBB and BBB-... that would equate to Baa2 and Baa3 for Moody's. That is the very high end of VWHEX credit quality... only 5.9% of VWEHX's junk bonds are Baa3 or higher, all the rest are lower with half in the Ba1-Ba3 range, which is BB+ to BB- in S&P speak.... much lower credit quality than my preferred portfolio.

So on the whole, my preferred portfolio is much higher credit quality than VWEHX based on ratings. Also, preferreds are typically two notches lower than the company long term debt and many of us are skeptical that the credit quality is that significantly different than company long-term debt.

JPM as an example. Subordinated debt is Moody's A3/S&P BBB+. Preferred is Moody's Baa2/S&P BBB-. I personally don't see a lot of difference in credit risk between JPM's subordinated debt compared to preferreds.... certainly not two notches worth.

So in my view, my BBB/BBB- portfolio is more similar to A-/BBB+risk realistically. So compared to VWEHV, I have a lot less credit risk and better yield.

Also, while my preferreds are in a tax-deferred account, if I held them in a taxable account most of the dividends would be qualified and get favorable tax treatment, which is not the case for VWHEX.

It's not often that I disagree with @pb4, but this attitude seems crazy to me. YTD numbers on all long bonds are probably up this year. And when interest rates go down (though there's not much room for that) they will be up again. But when rates rise (and they will), the water might get hot really fast.... my YTD return has been about 9.25%... so I'm pretty happy with the results. Come on in, the water is fine.

I don't really focus at all on total return for this portfolio... I mentioned the YTD return in the post only because VanWinkle mentioned the YTD total return of VWEHX... I view these totally as just income producing and that 5.75% given the credit risk is pretty attractive.

I'm cognizant of the interest rate risk, but less focused on it given my principal focus for this small portfolio is income and while I don't have data to prove it I suspect that the interest rate sensitivity isn't that different from Total Bond. Most of my remaining fixed income are 3.0-3.5% CDs... ~3x the preferred portfolio.... so arguably no interest rate risk there.

For callable preferreds the call price somewhat acts as a soft floor in that investors don't want to buy too far below call and risk a loss if the issue gets called.... or at least i know that I am very wary of buying very much below the call price and I suspect that other preferred invetors are as well.

These last few posts touch on some things that I find mysterious:

Junk bonds: Lots of talk/many threads here about risk and AA, moving money into the "fixed income" side because it is safer. Then, almost in the same breath, people talk about buying junk bonds for yield. But junk bonds are fairly highly correlated to stocks (0.71 I have read). So why not just adjust the AA so the risky stuff is in the equity tranche? Same-o for non-US bonds; why add risk by this method instead of just adding a little % on the equity side?

Preferred Stocks: Lots of talk in threads here about interest rate risk, recommendations to not buy long bonds. But a preferred is essentially an infinitely long bond, something I don't think has been mentioned in this thread. If long bonds are risky, what does this say about preferreds?

It's not often that I disagree with @pb4, but this attitude seems crazy to me. YTD numbers on all long bonds are probably up this year. And when interest rates go down (though there's not much room for that) they will be up again. But when rates rise (and they will), the water might get hot really fast.

We don't hold preferreds, but I would certainly suggest that those who do consider the longer term interest rate environment rather than, as some have mentioned, the last year or three's performance. Look at the late 1970s and early 1980s if you want to see some boiled frogs. A good jolt of inflation in the future will boil some more frogs IMO. Lots of internet stuff on our human inclination for recency bias, including https://www.morningstar.co.uk/uk/news/163017/why-recency-bias-is-dangerous-to-investors.aspx and https://fortune.com/2017/02/23/investment-psychology-recency-bias/ IMO with infinitely long bonds, recency bias is particularly pernicious.

Interesting. You're obviously deeper into it than I will ever be. All I ever knew about was callables and convertibles. I like simple things and over the years have developed skepticism about complex ones. Good luck.One can buy adjustable and 5 year reset preferreds which have an adjustment yield plus the base yield add on...Usually is off 5 yr TBill or Libor. Plus you can purchase term dated preferreds also, that mature. These can help mitigate upward concerns of interest rates. The preferred market is more varied than the typical perpetual preferred that most know of. I personally own perpetuals, term, resets, and adjustables.

The preferred market is more varied than the typical perpetual preferred that most know of. I personally own perpetuals, term, resets, and adjustables.

Yup. The more complicated the product, the more likely it is that the product was designed to make money for the seller not the buyer. That's why I just stay away from complex products and from investments that I don't understand.And issuers provide them in many flavors not because they are looking to provide additional benefits or less risk to investors who purchase them...it's for the issuer's benefit.

And issuers provide them in many flavors not because they are looking to provide additional benefits or less risk to investors who purchase them...it's for the issuer's benefit.

Yup. The more complicated the product, the more likely it is that the product was designed to make money for the seller not the buyer. That's why I just stay away from complex products and from investments that I don't understand.