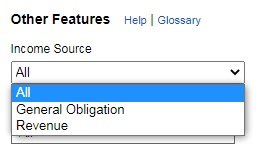

Other than the moodys/s&p ratings, are there filters in the brokerages tools to screen out the non-GO Munis? There are far too many offerings to manually research them all.

Fidelity does provide a checkbox to include/exclude GO vs. revenue munis.

Most of what you can utilize to screen will leave you with a set of bonds which fall under the "generalities" for weeding things out, which should lead to further investigation as opposed to simply jumping to the Buy button.

Looking at the high end of current yield (as opposed to the coupon) will obviously give you a reading on negative investor sentiment and what you might want to stay away from, and the opposite for low end of current yield. However, because the muni market is so illiquid, this often can be misleading, especially when it comes to retail investors and small lots. Efficient Market Hypothesis does not hold here.

For non-GO munis, a few things you can screen for that should give you positive or negative vibes include:

1. Escrowed and pre-refunded - about as safe as you can get. The money has been set aside for all future interest and principal at maturity payments. These funds have been transferred to an escrow agent (bank) that controls and manages the funds generally having them invested in government securities through redemption/maturity.

2. Bond Insurance - similar to FDIC for CDs, insured bonds come with an insurance policy which has been purchased by the issuer from one of the handful of muni bond insurers. This has a couple of angles to look at it from. First, you have insurance that if the bond defaults, the insurer will cover any shortfall. However, should there be a wave of muni defaults, it's possible that muni bond insurer(s) could fail. An issuer would need to purchase bond insurance if it were viewed as riskier, while a stronger issuer has no need to have insurance. The stronger issuer might be able to issue bonds at a lower coupon without the bond insurance, while a weaker one would not. So, again, though this can provide some guidance, deeper investigation should be taken.

3. Shorter maturities vs. longer ones. There is less risk in shorter term maturities for a number of reasons. First, current financials will immediately tell you if the issuer is financially able to make payments for the next, say, 1 to 5 years. An issuer which potentially has difficulties in that time frame will have already seen their bonds take a hit, providing red flags. Additionally, in general, most muni bond issues, especially those which have their maturity 20+ years out have larger/balloon payments in the final year or two of the bond issue. The payments/maturities in the earlier years are generally lower and easily handled. When those larger/balloon payment are dealt with, it's most often done through refinancing.

4. Material events - these should be considered for red flags. Missed filings, significant changes in operations/income/expenses (e.g. Covid-related things), rating changes, and so on. Generally, the broker's screening will not go into the material events. Fidelity provides a tab on the bond details, but you have to manually go through them. Using EMMA (emma.msrb.org) provides better query facilities for identifying munis and screening material events. The difficulty here is that querying from the EMMA side gives you bonds that exist, as opposed to querying from the broker side which is going to give bonds that are currently in inventory and being offered for sale. So, generally the process is to identify the bonds available for purchase through the broker's query facilities, then go to EMMA and spend some time looking at more detail.