FUEGO

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Nov 13, 2007

- Messages

- 7,746

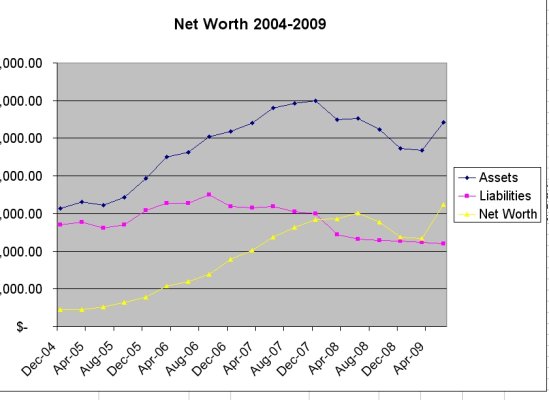

Is anyone else pleasantly surprised by their quarterly investment performance? How did you folks do in the second quarter of 2009? What is your asset allocation currently?

For reference, the Vanguard S&P 500 Index fund is up 16.0% for the quarter. the VG Total Market Index fund is up 16.9%. The VG Total International Index fund is up 27.3%. The VG Total Bond Market Index is up 1.7%.

I'll be the first to share. My total portfolio is up 25.9% for the quarter. This is with a portfolio that is virtually 100% equities, equally split between US and International, with a tilt towards small and value, plus some REITs.

For reference, the Vanguard S&P 500 Index fund is up 16.0% for the quarter. the VG Total Market Index fund is up 16.9%. The VG Total International Index fund is up 27.3%. The VG Total Bond Market Index is up 1.7%.

I'll be the first to share. My total portfolio is up 25.9% for the quarter. This is with a portfolio that is virtually 100% equities, equally split between US and International, with a tilt towards small and value, plus some REITs.

")