http://www.whitehouse.gov/sites/default/files/omb/assets/a11_current_year/s32.pdf

So here are the sources of the agency share, federal government for regular employees:

OASDIHI 7.65%

FERS 11.9%

TSP 5% of salary match max

Most expensive FEHB plan (2011) $875.29 biweekly (56% of $ 1558.25)

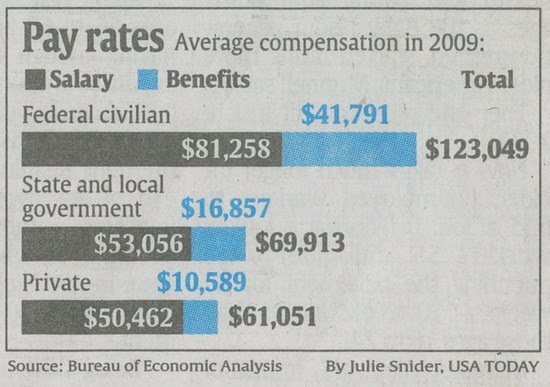

Which gives $42,706 in benefits if the employee maxes out TSP and selects a health plan with the highest cost to the government for a salary of $81,258.

Employee deductions:

OASDIHI 7.65%

FERS 0.8%

TSP 5% of salary to get the 5% match

Most expensive FEHB plan $682.96 biweekly

Gives the employee contribution to benefits of $28,686

(Brief note for anyone confused by the health plan (FEHB) - the number you usually hear for the government share is about 72% but this is an average. Plans above the average are lower than this.)

That's pretty close to the numbers in Midpack's post.

For comparison, the agency and employee cost for CSRS (the old system) is 7% each. There is no OASDI but the HI costs is 1.45% each. There is no TSP match. CSRS pensions are a little less than twice FERS pensions.

The employee share was set to create employee equity between the deductions of CSRS (7+1.45=8.45) and FERS (0.8+7.65=8.45). This is probably becoming less important as the last CSRS employees retire. Essentially you really have a retirement fund and any increases that have been needed have been expressed as agency share for FERS employee increases since this can float and the CSRS agency share is set. So to the extent that shortfalls due to CSRS occur, the agencies have covered these as FERS shortfalls. It didn't matter because the money is really going into the same pot from the same pot - government budgets to government retirement trust fund.

What is confusing to me is how a pension trust fund that operates this way could ever have unfunded liabilities. It could be that the future cost of retiree health care has not been properly accounted for in the prepay. How could the actuaries let that happen

?