Worthwhile article by Larry Swedroe:

https://www.advisorperspectives.com/articles/2022/04/25/which-asset-classes-protect-against-inflation

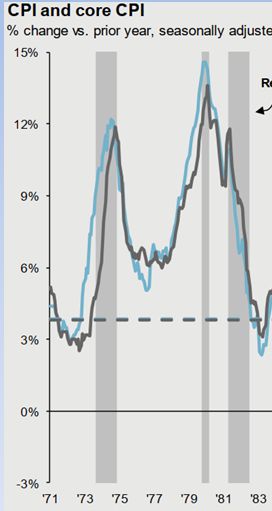

Not a whole lot of safe places to hide for the average investor it would seem. Diversifying equities seems to help (value doing "less worse" than growth, for example), even though (contrary to popular belief) equities aren't a good hedge against inflation except over very long periods (longer than the lifespan of a typical retiree or ever early retiree).

He does cite TIPS as one of the best options - WHEN their real yield is positive, which it isn't now. Seems to me there just isn't enough history (they've only been in existence in the U.S. for 25 years and have performed poorly during market crashes) for him to be so confident.

Easy to see why money is flowing into real estate and iBonds though.

https://www.advisorperspectives.com/articles/2022/04/25/which-asset-classes-protect-against-inflation

Not a whole lot of safe places to hide for the average investor it would seem. Diversifying equities seems to help (value doing "less worse" than growth, for example), even though (contrary to popular belief) equities aren't a good hedge against inflation except over very long periods (longer than the lifespan of a typical retiree or ever early retiree).

He does cite TIPS as one of the best options - WHEN their real yield is positive, which it isn't now. Seems to me there just isn't enough history (they've only been in existence in the U.S. for 25 years and have performed poorly during market crashes) for him to be so confident.

Easy to see why money is flowing into real estate and iBonds though.