aja8888

Moderator Emeritus

Heh, heh, and me sitting here with my un-COLA'd pension. Bummer!

Look at it this way, at least you have a pension. Many don't.

")

Heh, heh, and me sitting here with my un-COLA'd pension. Bummer!

For some reason I can't seem to grasp this. For example:

Person A - On Oct 1st has $100 they normally spend on groceries. On Oct 31 Person A bought brand name products and they had to spend $110. Person A has 10% inflation. The next 30 days Person A had to spend $112 so inflation over 2 months is now 12%.

Person B - On Oct 1st has $100 to spend on groceries. Person B buys the exact same items as Person A but decides to wait for sales, finds coupons to purchase their items. On Oct 31 Person B spent $90, therefore reducing their costs by $10. The next 30 days Person B had to spend after sales and coupons $93 so inflation did impact them.

It seems that Person B was able to reduce their personal inflation rate by using strategies Person A doesn't care about. How is that not reducing their personal inflation rate when they both end up purchasing the same exact products?

Got it. At least Person B has $19 more $ to do whatever with and didn't sacrifice any change in product selection but it did take some effort.Example absurdum:

If person B decided to not eat for the next 30 days, would they be experiencing price deflation?

No, they have changed their spending in RESPONSE to inflation.

According to one inflation calculator what cost $1 in 1973 cost $2.05 by the end of 1981. The value of the dollar cut in half in nine years.

Yeah and in 1982 they said a million dollars aint what it used to be. 40 years later a million dollars is worth even less, but the vast majority still don't have it. Think I'll take my million and live with the inflation. I won't get on TV with Robin Leach due to inflation, but I can still take care of my family. Unemployment has always been much more stressful for me than inflation, x4 when healthcare was totally tied to your job.

The social security COLA does not cause inflation, it is the result of inflation. I agree with you that we don't want to have entrenched high inflation because it is bad for society, but we can't change what has happened over the past year, and I'd like at least some chance to stay even. So I will take my raise with a clear conscience.

I've seen your co-worker's thought process before -- "I don't want to earn more money, because I'll just pay more taxes" - and I find it baffling. Unless the marginal tax rate exceeds 100%, more money is always better. I will concede that there are certain income "cliffs" in the tax code where the marginal rate could exceed 100% over a small range (IRMAA, ACA), but that is rare. Now, on the job, one could reasonably conclude that the marginal value of extra income is not worth the extra time needed to earn it, but that's a different issue.

Is Robin Leach even still around??

Look at it this way, at least you have a pension. Many don't.

Let's see if I beat Gumby

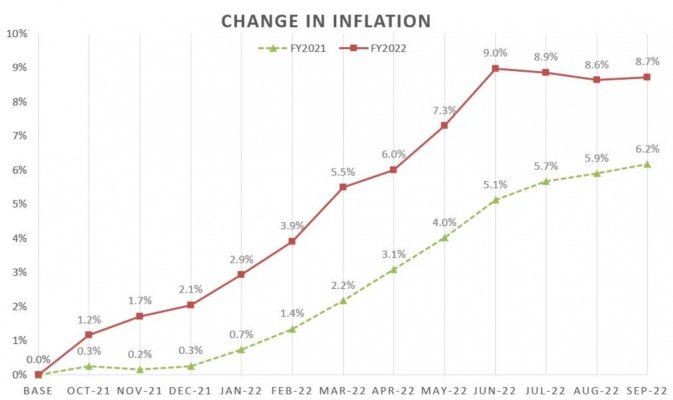

8.7%

jdavid47 beat me to it this morning. See post #259Did I miss something, did I miss the "Official" Gumby SS COLA increase number?

)

)jdavid47 beat me to it this morning. See post #259

Yes, I saw it!

^ + 1.0878.7%, Wahoo!!!

(Yeah, I slept late! But what a nice bit of info to wake up to.

Originally Posted by Gumby

jdavid47 beat me to it this morning. See post #259

That's true. I'll shut up next year.Ha Ha, but it is not Official unless reported by you.