The 10th edition of A Random Walk Down Wall Street comes out next month, and Burton Malkiel has an article in today's WSJ defending buy-and-hold investing (across a diversified asset allocation) against a new generation of believers in market timing/active management. From the article:

I was lucky to happen on a copy of A Random Walk about 25 years ago. It probably saved me from making a lot of mistakes. IMO, even those who are die-hard market timers and stock pickers would be well advised to give it a read. It's a book that's likely to come up an any active/passive investing debate, and it's good to know the "other side's" arguments if possible.

In the wake of the recent financial crisis, many investors believe that the traditional methods of portfolio management don't work anymore. They think that "buying and holding" is outdated, and that success depends on skillful timing. Diversification no longer works, they argue, because all asset classes move up and down together, especially when stock markets fall. In other words, diversification fails us just when we need it most. . .

I don't agree with any of these arguments. The timeless investment maxims of the past remain valid. Indeed, their benefits may be even greater today than ever before.

. . . Buy and hold investors in the U.S. stock market made an average annual return of 8% during the 15 years from 1995 through 2009. But if they had missed the 30 best days in the market over that period, their return would have been negative. Market strategists called for a sharp market decline in late August 2010 as technical indicators were uniformly bearish. The market responded with its best September in decades.

[Discussion of DCA and rebalancing]

For example, suppose an investor was most comfortable choosing an initial allocation of 60% equities, 40% bonds. From 1996 through 1999, annually rebalancing such a portfolio improved its return by 1 and 1/3 percentage points per year versus a strategy of making no changes. Diversification has not lost its effectiveness. Over the past several years, when stocks went down, bonds went up, preserving the value of the portfolio. And while stock markets around the world have tended to rise and fall together, there were huge differences in regional returns. . . Even though portfolios in the U.S. market actually lost money in the first decade of the 21st century, emerging-market stocks enjoyed returns of more than 10% per year. Every portfolio should have substantial holdings in the fast-growing emerging economies of the world.

Low-cost passive (index-fund) investing remains an excellent strategy for at least the core of every portfolio. Even if markets may not always be efficiently priced, index funds must produce above-average returns after costs. All the stocks in the market must be held by someone. Therefore, if one active portfolio manager is holding the better-performing stocks, then some other active manager must be holding those with below-average returns.

. . . .

The evidence is clear. Low-cost index funds regularly outperform two-thirds of actively managed funds, and the one-third of actively managed funds that outperform changes from period to period. Even the very few professional investors who have beaten the market over long periods of time—Berkshire Hathaway's Warren Buffett and Yale University's David Swensen, for instance—are quick to advise that investors are likely to be much better off with simple low-cost index funds than with expensive actively managed funds.

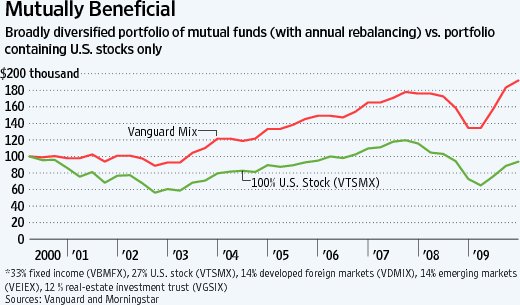

The chart nearby illustrates how someone who invested $100,000 at the start of 2000 and, following my advice, used index funds, stayed the course and rebalanced once a year, would have seen that investment grow to $191,859 by the end of 2009. At the same time, someone buying only U.S. stocks would have seen that same investment decline to $93,717.

The recommended index-fund portfolios contain bonds, U.S. stocks, foreign stocks (including those from emerging markets) and real-estate securities. The diversified portfolio, annually rebalanced, produced a satisfactory return even during one of the worst decades investors have ever experienced. . . .

If you ignore the pundits who say that old maxims don't work and you follow the time-tested techniques espoused here, you are likely to do just fine, even during the toughest of times.

I was lucky to happen on a copy of A Random Walk about 25 years ago. It probably saved me from making a lot of mistakes. IMO, even those who are die-hard market timers and stock pickers would be well advised to give it a read. It's a book that's likely to come up an any active/passive investing debate, and it's good to know the "other side's" arguments if possible.