jetpack

Recycles dryer sheets

- Joined

- Aug 2, 2013

- Messages

- 437

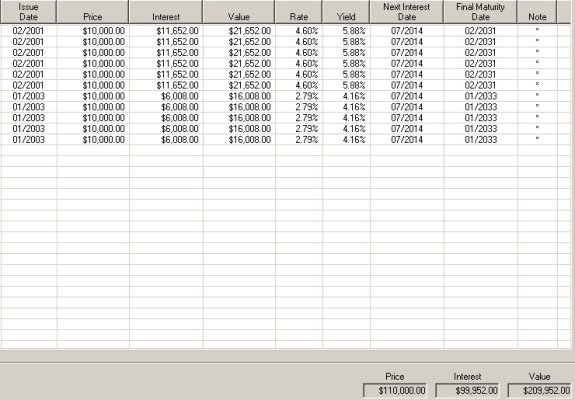

For various reasons, I have a quite a bit of short term cash. I'm not putting it all in the market at the moment, but I do need it readily available.

In the past I've just used a prime money market.. but, they currently yield about 0.02% (not 2%)

So, am I just left with "high yield" savings accounts.. Is there a better option that's very safe?

In the past I've just used a prime money market.. but, they currently yield about 0.02% (not 2%)

So, am I just left with "high yield" savings accounts.. Is there a better option that's very safe?