Focus

Full time employment: Posting here.

- Joined

- Oct 10, 2009

- Messages

- 640

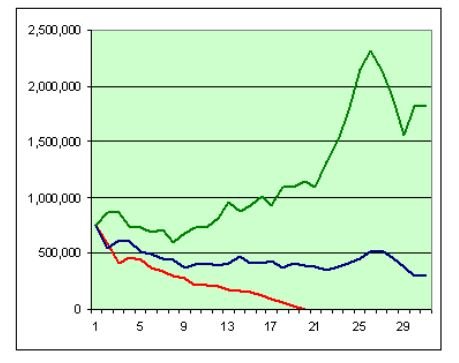

Wade Pfau's posts are always interesting and thought provoking. Here's the latest, on sequence of returns risk.

This isn't news to most forum members, but nevertheless the implications are profound. Many of us hope that doing all the "right" things (e.g., diversifying in every way possible) will dampen the effects of volatility and allow us to exert some control over our financial future. But ultimately timing appears to override everything for those of us who are invested in the market. I think this is why ER often feels like a leap of faith.

At the end, Pfau offers these suggestions on how to de-risk: 1) Strengthen Social Security (and avoid turning it into defined contribution), 2) Avoid constant inflation-adjusted spending, 3) Consider holding fixed income assets to maturity or using annuities, 4) Consider reducing downside risk through other approaches, including financial derivatives, 5) Consider rising-equity glidepath, 6) Consider "safe savings rate" approach.

These are very different outcomes for people who otherwise behaved exactly the same. ... The actual maximum sustainable withdrawal rates experienced over 30-years ranged anywhere from 1.9% to 10.9% for reasons beyond one's control reflected simply by the luck of when they retired.

This isn't news to most forum members, but nevertheless the implications are profound. Many of us hope that doing all the "right" things (e.g., diversifying in every way possible) will dampen the effects of volatility and allow us to exert some control over our financial future. But ultimately timing appears to override everything for those of us who are invested in the market. I think this is why ER often feels like a leap of faith.

At the end, Pfau offers these suggestions on how to de-risk: 1) Strengthen Social Security (and avoid turning it into defined contribution), 2) Avoid constant inflation-adjusted spending, 3) Consider holding fixed income assets to maturity or using annuities, 4) Consider reducing downside risk through other approaches, including financial derivatives, 5) Consider rising-equity glidepath, 6) Consider "safe savings rate" approach.

YMMV

YMMV