wabmester

Thinks s/he gets paid by the post

- Joined

- Dec 6, 2003

- Messages

- 4,459

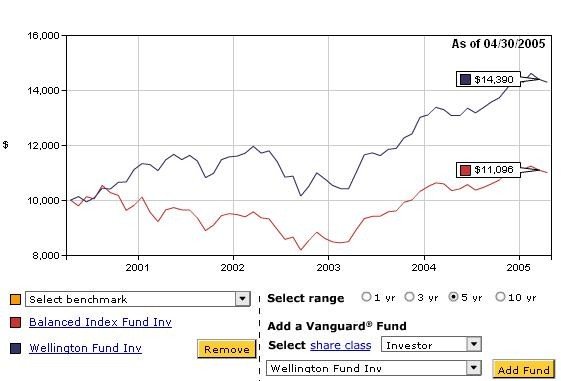

OK, I took your best-case return differences (5 year) and compared VBIAX (60/40 balanced) with Wellington (also about 60/40), and this is what I got:

I was comparing admiral shares. Wee, this is fun. Here's a comparison of investor shares:th said:You picked the wrong symbol. Wellington is VWELX, not VWENX.

")

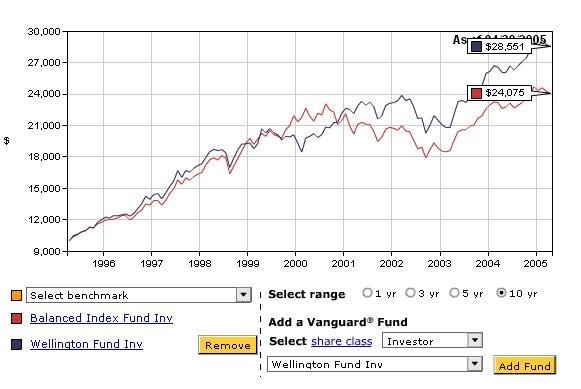

Yeah, you're right. It says that stocks have sucked for the last 5 years.th said:That a 35/65 fund is whomping a 60/40 really says something...

This helps in getting-out abit sooner... eh?greenhm said:Thanks for all your comments...

Here are the numbers... hope it makes sense...

Year 1

bought $100000 phone-company stock for 25$ per share

I now own 4000 shares

The bank pays $1 for each share this year as a dividend

I will now get $4000 in dividends this year

That equates to 4% annual yield or 4% return on investment.

Year2

I still own 4000 shares

The phone-company pays $1.10 for each share this year as a dividend (10% div increase)

I will now get $4400 in dividends this year

That equates to 4.4% annual yield or 4.4% return on investment.

3% inflation this year means I need 4120 [4000 + 3%]

I received $4400. An increase of $380.

Year3

I still own 4000 shares

The phone-company pays $1.21 for each share this year as a dividend (10% div increase)

I will now get $4840 in dividends this year

That equates to 4.84% annual yield or 4.84% return on investment.

3% inflation this year means I need 4243.6 [4120 + 3%]

I received $4840. An increase of $596.40

... and so on

I care only for the dividends the co pays. The actual share price is of no value.

Does this make sense?