Anyway, something to read here... find the chart that fits.

The Average Net Worth For The Above Average Person | Financial Samurai

The Average Net Worth For The Above Average Person | Financial Samurai

I kept my first microwave for about 25-30 years. It was HUGE. I kept hoping it would break, but it never did. Finally I just declared it dead and took it to the dump (for interior decorating reasons, and to reclaim counter space, not because it ever quit working). If anybody found it there and took it home, it is probably still working. They just never die. Zombie microwaves from H*ll; might make a good movie.

I kept SONY CRT TV until few months ago. I am no longer a young guy (as I was when I bought it 20 years ago)

I kept my first microwave for about 25-30 years. It was HUGE. I kept hoping it would break, but it never did. Finally I just declared it dead and took it to the dump (for interior decorating reasons, and to reclaim counter space, not because it ever quit working). If anybody found it there and took it home, it is probably still working. They just never die. Zombie microwaves from H*ll; might make a good movie.

Anyway, something to read here... find the chart that fits.

The Average Net Worth For The Above Average Person | Financial Samurai

Here's a summary of Fed data on income and net worth (second table down), including by age group:

A Look at Household Net Worth and Household Income By Age Group from the 2010 Survey of Consumer Finances

I believe this is the source:

FRB: 2010 SCF

Senator, the answer is no: Early Retirement & Financial Independence Community - Net Worth Poll

Looks like ~50% have less than $2M, the minimum amount necessary to reach "multi" status.

I thought I was the only "kook" like this. I had a Magnavox portable non-cable ready, rotary clicky dial, that was my main "home entertainment" piece from 1984 to 2004

This is very true. I feel blessed at the age of 41 to have investable assets of 2.5M. It would be interesting to see stats on net worth based on age.

A quick look at the above sources and a comparison with the poll on this forum shows that respondents to the poll have just a tad above average net worth, assuming an average age of 60. Of course, one expects that people who frequent ER forums tend to be frugal and have had some reasonable savings.

Excellent! Did it have a 'fine-tuning' knob too?

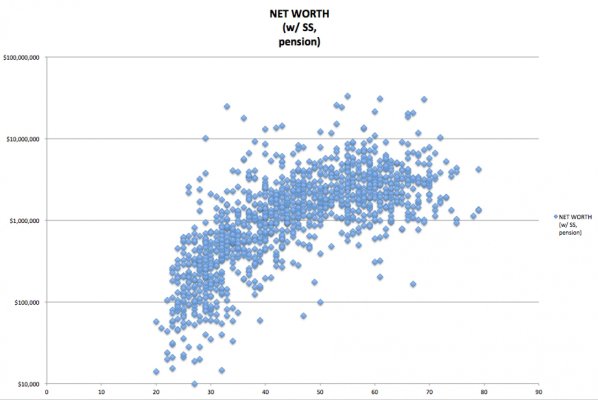

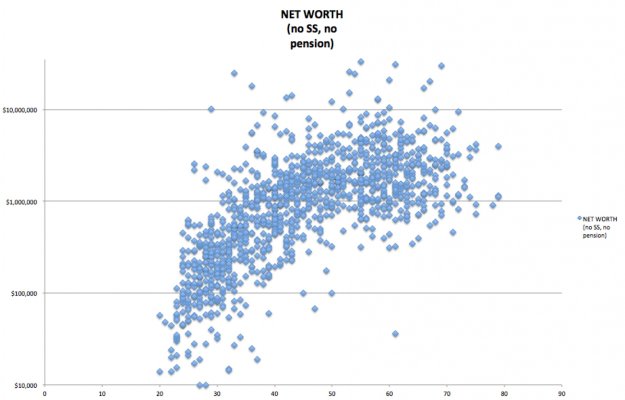

There's always the bogleheads net worth by age survey:

Bogleheads • View topic - Improved Net Worth by Age [and plot]

At 41 the median with SS/pension is 1.2M. Like this forum, even the median poster would be an outlier compared to the average american.

What's interesting is that the net worth curve appears to flatten after 3-4M. Perhaps people start spending down/gifting the money at this point?

Yes, but keep in mind that not all of us are still accumulating and/or in the right sector for the recent years.The net worth poll referenced in REWahoo's post is 3 years old. Given the strong returns in the stock market of the past 3 years, many of us might be much better off now.

The net worth poll referenced in REWahoo's post is 3 years old. Given the strong returns in the stock market for the past 3 years, many of us might be much better off now.

Yes, but keep in mind that not all of us are still accumulating and/or in the right sector for the recent years.

Looks like they count pension, and SS too, from the chart label.

Yes, but keep in mind that not all of us are still accumulating and/or in the right sector for the recent years.

There's always the bogleheads net worth by age survey:

Bogleheads • View topic - Improved Net Worth by Age [and plot]

At 41 the median with SS/pension is 1.2M. Like this forum, even the median poster would be an outlier compared to the average american.

What's interesting is that the net worth curve appears to flatten after 3-4M. Perhaps people start spending down/gifting the money at this point?

Well, Honey Boo Boo is a bit young for this forum.I'll go out on a limb and suggest that the ER crowd here is not the Honey Boo Boo target audience...

But how does one discount something that he will not be able to get for another 2 decades, like your "typical" 41 year old Boglehead?

Maybe they're just retiring and making withdrawals? It could also show the effects of the different investing time frames experienced by people of different ages.

I am puzzling about the 2 mil plus group, why they didn't retire sooner?? I guess they have a high expense life style or something. Since I am in the "frugal" category 2 mill plus seems gigantic.

And here's what we all should have:

Here Is The Income Level At Which Money Won't Make You Any Happier In Each State

Looks like $75k (household income) works for most states, but some states need much more and some can do with less. Use your favorite multiplier to figure out a corresponding net worth.

Back when China economy was still in the Dark Ages, childbirth limit might have made sense. Now, they are worrying about having a boatload of retirees without the support of workers. A couple (2 persons) down to one child. That single child has to change his/her parents' diapers while also works in the farm for food, builds gadgets in factories, then drives trucks to make Amazon-like deliveries to the non-producing geezers. I pity that younger generation. Or perhaps not, as they may just revolt and leave the geezers out to rot.

The same thing happens if there are too many savers and early retirees like people in this forum. Somebody has to work and to buy "stuff", so that corporations can make money and send out dividends to us.

See: Paradox of thrift - Wikipedia, the free encyclopedia.

Speaking of crazy but true...I know a retired couple in their late 50s who owe more money on their house now than they did when it was purchased in the 80s and have no savings. But they are comfortably retired. How? Well they have over $100k a year in pensions with COLAs. As long as the checks keep coming, they are just fine. I know several people that have retired or are going to retire that way.

$100,000 a year in pension checks with a COLA is one heck of a phantom asset.