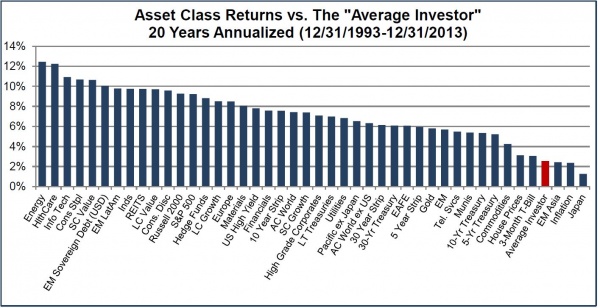

There's been a little discussion of this recent article by John Greaney in a couple of threads about other topics, but it seems to me to be worthy of its own:

2014 Update: Real-Life Retiree Investment Returns

It's a lengthy post backed up with lots of spreadsheets, but there are some choice nuggets to be found.

A couple that struck me:

1. In comparing a plain vanilla Bogleheads 60:40 portfolio to a sophisticated DFA-style slice-and-dice Modern Portfolio Theory one, Greaney says (with typical irreverence):

"While the MPT portfolio value has trailed the simple S&P500/fixed income portfolio (No. 1 above) by 19% as of Dec 31, 2014, advocates of this approach like its reduced volatility and sterling academic recommendations. Which brings us to an important investing truism -- it's OK to under perform as long as you're pleased with the results and proud of what you are doing."

2. Most important (to me, anyway, since I ER'd in 2002), Greaney, who ER'd in 1994, points out that someone retiring in 2000 or later would have a very different perspective on which portfolios are viable:

"If you happened to retire in January 2000, the last fourteen years haven't been pleasant. Only the Warren Buffett portfolio and Harry Browne Portfolio has a value appreciably exceeding its $100,000 starting balance. The 100% fixed income portfolio is underwater while the MPT portfolio, Larry Swedroe Portfolio and Harry Dent Portfolio are all 15% to 20% in the black. The other two portfolios both show losses. The worst performer was the 75% S&P500/25% fixed income portfolio which is now less than two-thirds of its starting value."

There'll probably be as many take-aways from this as there are readers of his post, but I find it interesting how well some of the purely defensive portolios such as Browne'e Permanent Porfolio and Swedroe's have done. Greaney's figures are also based on 4% SWR PLUS inflation, and I continue to feel much more comfortable going with 3-4% of actual porfolio balance as of January 1 each year (or Bob Clyatt's 95% rule in years of steep market declines).

Great to see John Greaney still writing - and don't miss his just-published piece on the same site on Vanguard's new financial advisor service. He's a really merciless advocate for low costs - John Bogle would be proud!

2014 Update: Real-Life Retiree Investment Returns

It's a lengthy post backed up with lots of spreadsheets, but there are some choice nuggets to be found.

A couple that struck me:

1. In comparing a plain vanilla Bogleheads 60:40 portfolio to a sophisticated DFA-style slice-and-dice Modern Portfolio Theory one, Greaney says (with typical irreverence):

"While the MPT portfolio value has trailed the simple S&P500/fixed income portfolio (No. 1 above) by 19% as of Dec 31, 2014, advocates of this approach like its reduced volatility and sterling academic recommendations. Which brings us to an important investing truism -- it's OK to under perform as long as you're pleased with the results and proud of what you are doing."

2. Most important (to me, anyway, since I ER'd in 2002), Greaney, who ER'd in 1994, points out that someone retiring in 2000 or later would have a very different perspective on which portfolios are viable:

"If you happened to retire in January 2000, the last fourteen years haven't been pleasant. Only the Warren Buffett portfolio and Harry Browne Portfolio has a value appreciably exceeding its $100,000 starting balance. The 100% fixed income portfolio is underwater while the MPT portfolio, Larry Swedroe Portfolio and Harry Dent Portfolio are all 15% to 20% in the black. The other two portfolios both show losses. The worst performer was the 75% S&P500/25% fixed income portfolio which is now less than two-thirds of its starting value."

There'll probably be as many take-aways from this as there are readers of his post, but I find it interesting how well some of the purely defensive portolios such as Browne'e Permanent Porfolio and Swedroe's have done. Greaney's figures are also based on 4% SWR PLUS inflation, and I continue to feel much more comfortable going with 3-4% of actual porfolio balance as of January 1 each year (or Bob Clyatt's 95% rule in years of steep market declines).

Great to see John Greaney still writing - and don't miss his just-published piece on the same site on Vanguard's new financial advisor service. He's a really merciless advocate for low costs - John Bogle would be proud!

")