Stormy Kromer

Thinks s/he gets paid by the post

- Joined

- Oct 1, 2017

- Messages

- 1,159

How do you win?

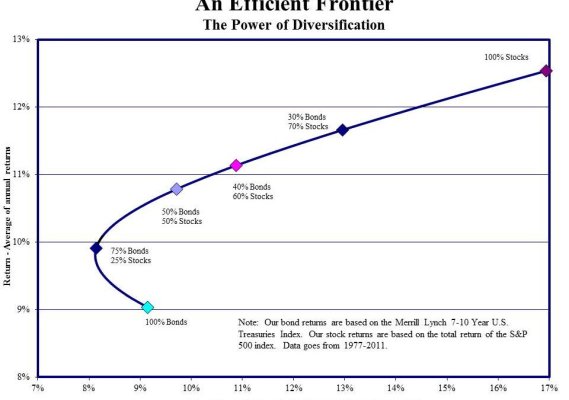

Since I started investing at age 22 in 1987 I have been preached to include bonds as a part of my portfolio. Now at age 59 I am supposed to have about 40% of my money in bonds.

The 10 year rate of return for bonds is 1.61. SP 500 is 12.58.

So 40% of my portfolio is a boat anchor. I realize the SP 500 funds are more volatile. But not as risky over 5 or more years.

I think bond issuers are laughing at people who buy them. I knew a wealthy, wise old man tell me "If you like a business enough to buy their debt....you should buy their equity instead."

You buy a bond at a nice interest rate. Rates go down and they call in your bond. You buy a bond and rates go up and you're stuck with a lower performing fixed income instrument. Neither are FDIC insured and when a company declares bankruptcy does anyone know when a bond holder actually collected more than a stockholder? Down the drain is down the drain..... Bond or stock.

For those that need fixed income I'd recommend VG MM fund. 5% plus is pretty darn good.

I know many, many people who have gotten wealthy investing in stock equities and real estate. Not a one by investing in bonds.

My rant on bonds is over. I'll duck now.

Since I started investing at age 22 in 1987 I have been preached to include bonds as a part of my portfolio. Now at age 59 I am supposed to have about 40% of my money in bonds.

The 10 year rate of return for bonds is 1.61. SP 500 is 12.58.

So 40% of my portfolio is a boat anchor. I realize the SP 500 funds are more volatile. But not as risky over 5 or more years.

I think bond issuers are laughing at people who buy them. I knew a wealthy, wise old man tell me "If you like a business enough to buy their debt....you should buy their equity instead."

You buy a bond at a nice interest rate. Rates go down and they call in your bond. You buy a bond and rates go up and you're stuck with a lower performing fixed income instrument. Neither are FDIC insured and when a company declares bankruptcy does anyone know when a bond holder actually collected more than a stockholder? Down the drain is down the drain..... Bond or stock.

For those that need fixed income I'd recommend VG MM fund. 5% plus is pretty darn good.

I know many, many people who have gotten wealthy investing in stock equities and real estate. Not a one by investing in bonds.

My rant on bonds is over. I'll duck now.