corn18

Thinks s/he gets paid by the post

- Joined

- Aug 30, 2015

- Messages

- 1,890

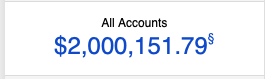

First time I have ever seen this in my account summary

Today for the first time my assets (ignoring tax due in April) reached 90% of that original target FIRE number. Yay!

+495

I absolutely love your attitude. Thank you for making my day.

") My 457 is close behind and with another few good days will be over the mark as well.

My 457 is close behind and with another few good days will be over the mark as well.I had that same app on my phone. You're so close!I broke the 200-day mark! It's starting to feel real.

Today, at 58, was my first day in retirement.Still not sunk in but it's a strange feeling to think no more working for a living and I now get up when when I want.

It's a bit scary to start retirement with our country and world in such mayhem but the DW is younger and going to work at least another year so that helps.

Today, at 58, was my first day in retirement.Still not sunk in but it's a strange feeling to think no more working for a living and I now get up when when I want.

It's a bit scary to start retirement with our country and world in such mayhem but the DW is younger and going to work at least another year so that helps.

Congrats! Sounds like y'all are close. It's a great feeling.Crazy times we’re living in right now! DH is starting to get serious about retiring in 5 years since work has been very stressful lately and he doesn’t know how much more he can take.

We hit our personal NW goal of $3 million back in Dec. when DH turned 50, with $2 million in investable assets. I think if we can reach $3 million in investable assets, we’d be good to go.

Crazy times we’re living in right now! DH is starting to get serious about retiring in 5 years since work has been very stressful lately and he doesn’t know how much more he can take.

We hit our personal NW goal of $3 million back in Dec. when DH turned 50, with $2 million in investable assets. I think if we can reach $3 million in investable assets, we’d be good to go.