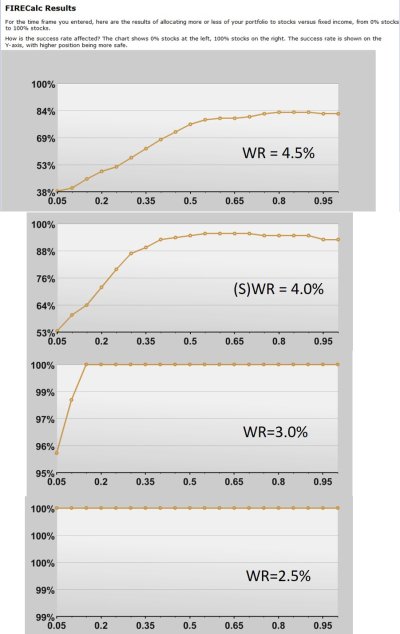

Here's the investment plan our advisor at Vanguard is suggesting.

What changes do you suggest?

Does international bond fund really add value or could it be eliminated? Why do we need it?

We will be managing our portfolio ourselves after the advisor helps us set it up.

STOCKS – 50 %

Vanguard Total U.S Stock Market Index Fund Admiral Shares - VTSAX

Vanguard Total International Stock Index Fund Admiral Shares – VTIAX

BONDS – 50%

Vanguard Total U.S. Bond Market Index Fund Admiral Shares - VBTLX

Vanguard Short-Term Investment-Grade Fund Admiral Shares - VFSTX

Vanguard Intermediate Term Investment-Grade Fund Admiral Shares - VFICX

Vanguard Total International Bond Index Fund Admiral Shares – VTABX

PORTFOLIO PERCENTAGES

U.S. large-cap stock - 20%

U.S. mid/small-cap stock - 9%

International stock - 20%

U.S. short-term bond - 14%

U.S. intermediate-term bond - 18%

U.S. long-term bond - 4%

International bond - 15%

U.S. short term reserves - Vanguard Prime Money Market Fund - 0%

Thanks for your knowledge and experience,

Goldenmom

What changes do you suggest?

Does international bond fund really add value or could it be eliminated? Why do we need it?

We will be managing our portfolio ourselves after the advisor helps us set it up.

STOCKS – 50 %

Vanguard Total U.S Stock Market Index Fund Admiral Shares - VTSAX

Vanguard Total International Stock Index Fund Admiral Shares – VTIAX

BONDS – 50%

Vanguard Total U.S. Bond Market Index Fund Admiral Shares - VBTLX

Vanguard Short-Term Investment-Grade Fund Admiral Shares - VFSTX

Vanguard Intermediate Term Investment-Grade Fund Admiral Shares - VFICX

Vanguard Total International Bond Index Fund Admiral Shares – VTABX

PORTFOLIO PERCENTAGES

U.S. large-cap stock - 20%

U.S. mid/small-cap stock - 9%

International stock - 20%

U.S. short-term bond - 14%

U.S. intermediate-term bond - 18%

U.S. long-term bond - 4%

International bond - 15%

U.S. short term reserves - Vanguard Prime Money Market Fund - 0%

Thanks for your knowledge and experience,

Goldenmom