Hello everyone,

I have started to research well-known investment strategies. I have come across various very different strategies, such as:

- The Two-Fund Portfolio: (50% Vanguard Total World Stock Index Fund (VT) + 50% Vanguard Total Bond Market (BND))

- Warren Buffett's 90/10 portfolio: (90% Vanguard S&P 500 ETF (VOO) + 10% Vanguard Short-Term Treasury ETF (VGSH))

- The Three-Fund Portfolio: (33% Vanguard Total World Stock Index Fund (VT) + 33% Vanguard Total Bond Market (BND) + 33% Vanguard Total International Stock Market Fund (VXUS))

- Four Corners Portfolio: (25% Vanguard Growth Index Fund Admiral Shares (VIGAX) + 25% Vanguard Value Index Fund Admiral Shares (VVIAX) + 25% Vanguard Small-Cap Growth Index Fund Admiral Shares (VSGAX) + 25% Vanguard Small Cap Value Index Fund Admiral Shares (VSIAX))

- etc.

Do you use one of these strategies? Or do you use other well-known investment strategies? If so, why do you use this specific strategy?

[MOD EDIT]

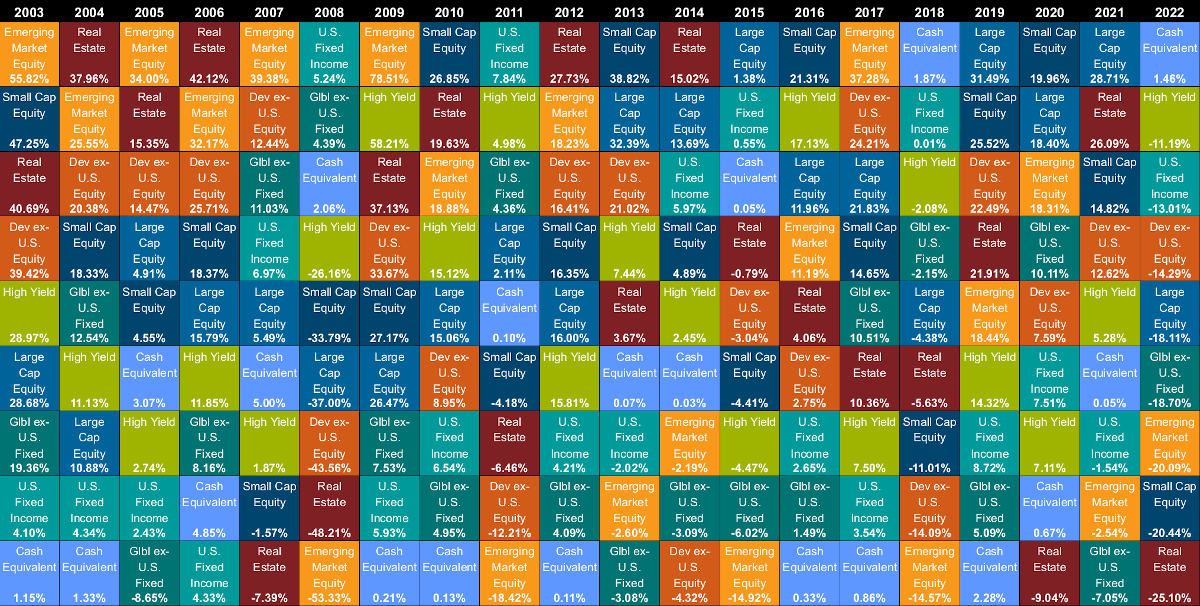

I would like to test which strategies work how well against the S&P500. Since I would like to decide on a strategy.

I thank you in advance!

I have started to research well-known investment strategies. I have come across various very different strategies, such as:

- The Two-Fund Portfolio: (50% Vanguard Total World Stock Index Fund (VT) + 50% Vanguard Total Bond Market (BND))

- Warren Buffett's 90/10 portfolio: (90% Vanguard S&P 500 ETF (VOO) + 10% Vanguard Short-Term Treasury ETF (VGSH))

- The Three-Fund Portfolio: (33% Vanguard Total World Stock Index Fund (VT) + 33% Vanguard Total Bond Market (BND) + 33% Vanguard Total International Stock Market Fund (VXUS))

- Four Corners Portfolio: (25% Vanguard Growth Index Fund Admiral Shares (VIGAX) + 25% Vanguard Value Index Fund Admiral Shares (VVIAX) + 25% Vanguard Small-Cap Growth Index Fund Admiral Shares (VSGAX) + 25% Vanguard Small Cap Value Index Fund Admiral Shares (VSIAX))

- etc.

Do you use one of these strategies? Or do you use other well-known investment strategies? If so, why do you use this specific strategy?

[MOD EDIT]

I would like to test which strategies work how well against the S&P500. Since I would like to decide on a strategy.

I thank you in advance!

Last edited by a moderator:

")