OrcasIslandBound

Recycles dryer sheets

...and the BOD continues to squander huge $$$ on ceo pay, perks, and lawyers.

And $25,000,000 severance packages.

...and the BOD continues to squander huge $$$ on ceo pay, perks, and lawyers.

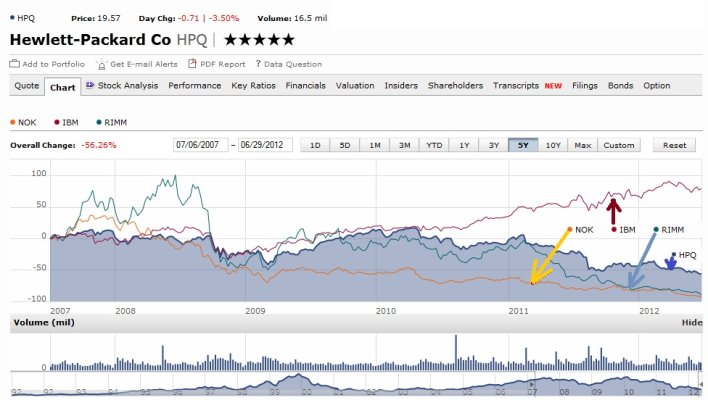

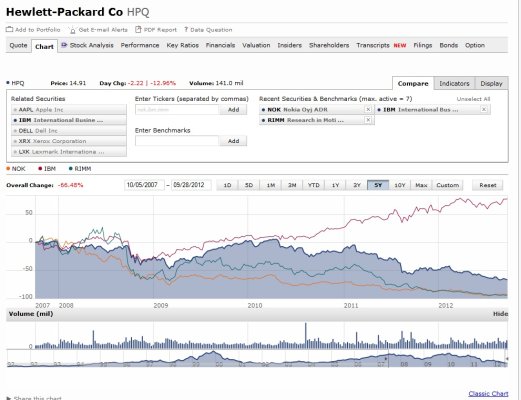

This has got to be the most hated stock I have ever seen. Everything I watch and everything I read about it is negative to the max!

The forward P/E is 4.6 now!

I'm up to 280 shares and plan to buy more as soon as I get paid for the month. Look at the numbers and forget the stupidity of the higher ups. This company is so oversold its hilarious.

Ok, at this price I have say it is looking a bit more interesting. I think my strategy will be to write a put at say $20/share. The Jan are ~1.70 but it is also tempting to take advantage of the volatility and write the Jan 2013 (16 month) which are selling for $3.80. The company has roughly $6/share in cash which means that that if the options get exercised I'll be buying the companies business for roughly $10/share.

Another fine, family-run company that hired a succession of empty suits after the founders retired/passed away. The current guy at HP started this year saying how he was going to go after Apple in the consumer space and then within six months, it's all about corporate services. In other words, he doesn't have a clue and he's playing catch-up, but he can afford to because his salary and bonuses are nicely backed up by the cash cow which is their printer business.

But don't they also have ~ $12/share of debt, so isn't that like negative $6 cash?

HPQ Key Statistics | Hewlett-Packard Company Common Stock - Yahoo! Finance

I recall a time when people were trying to figure the value of Apple (AAPL) adjusted for its then large (but not staggeringly large like today) cash holdings (and zero debt). But back then, they could get 4-5% on their cash, so you had to back the interest out of their income. It got interesting. IIRC, they were making more in interest for a time than they were from operations.

At any rate, this thread has motivated me and I sold a few SEPT $23 strike puts, and now sold $22 strike puts for OCT. Got a bit over $0.90 for each. I'm kind of ambivalent as to whether I get assigned or not, but I'll keep playing as long as the premiums are this high. I like to play the near month though - the premiums are relatively higher, and my crystal ball only has to look a month out.

-ERD50

I've been applying the same logic to selling Berkshire Hathaway puts. We'll have to talk more about this!Those premiums are crazy high because of the huge uncertainty of both the market and the company. I'm going to have to put my thinking cap on.

ESRwannabe said:This has got to be the most hated stock I have ever seen. Everything I watch and everything I read about it is negative to the max!

The forward P/E is 4.6 now!

I'm up to 280 shares and plan to buy more as soon as I get paid for the month. Look at the numbers and forget the stupidity of the higher ups. This company is so oversold its hilarious.

Anyone considering owning HP stock might read this article:

How Hewlett-Packard lost its way - Fortune Tech

called

How Hewlett-Packard lost its way

May 8, 2012: 5:00 AM ET Léo Apotheker's disastrous tenure as HP's CEO revealed a dysfunctional company struggling for direction after a decade of missteps and scandals. Can his replacement, Meg Whitman, fix the tech giant?

By James Bandler with Doris Burke

So, I have 620 shares of HPQ now and plan to have 1,000 shares by the end of the year. I feel quite good about the investment and think the shares are cheap. They could always go lower of course.

HP is not just a printer or PC company any longer. A significant chunk of revenue now comes from IT services (read outsourcing) via the Electronic Data Systems acquisition. Be sure you understand performance of the Enterprise Services part of the business when making your investing decision.

Thanks swifter, that was a fascinating read. Depressing too!Anyone considering owning HP stock might read this article:

How Hewlett-Packard lost its way - Fortune Tech

called

How Hewlett-Packard lost its way

May 8, 2012: 5:00 AM ET Léo Apotheker's disastrous tenure as HP's CEO revealed a dysfunctional company struggling for direction after a decade of missteps and scandals. Can his replacement, Meg Whitman, fix the tech giant?

By James Bandler with Doris Burke