donheff

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

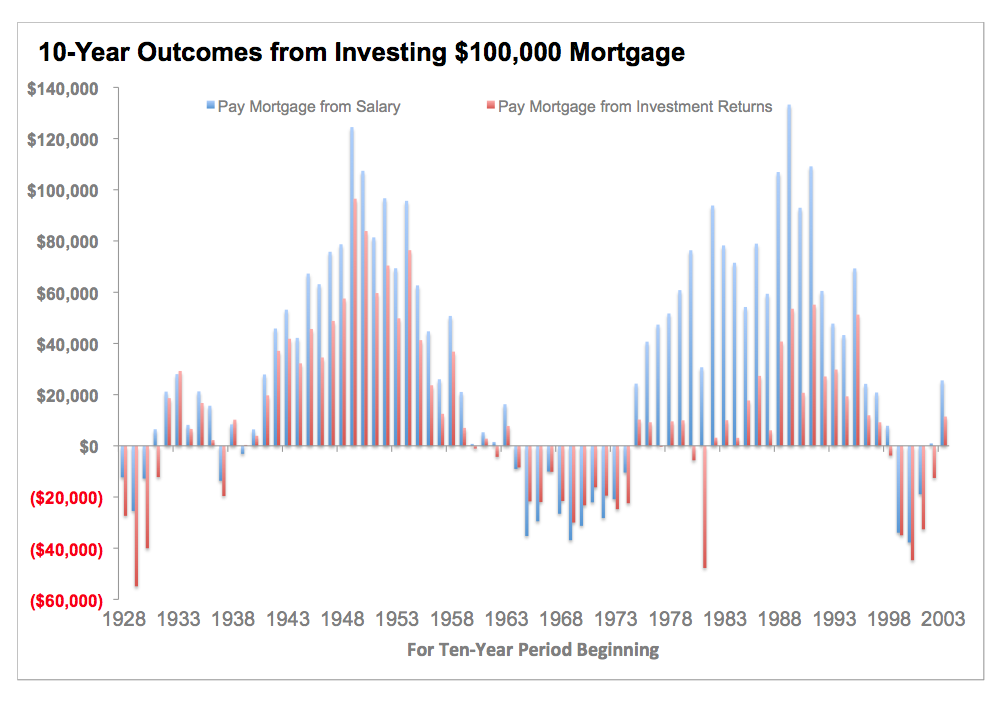

This article does a nice job of graphically laying out the historical impact of taking a mortgage in retirement and investing the difference. The author shows the substantial differences in outcome when the mortgage is paid off from the portfolio vs paid of from salary (leaving the portfolio untouched). I suspect that he doesn't figure in the fact that the person who pays off from salary could have/would have invested the equivalent amounts over time absent the mortgage so the differences may be overstated. Nevertheless it is a useful article for those contemplating the pay off or not decision. Here is a chart showing the outcomes: