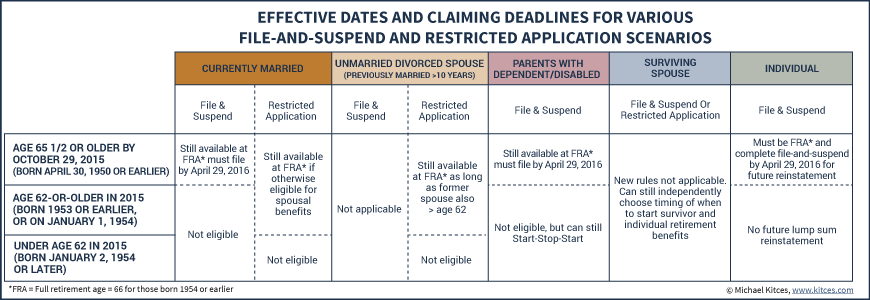

Argh...I'm now talking to an SS agent after waiting 40 min. because they don't have an on-line appointment scheduler. I (62) just filed for SS yesterday. DH (69) wants to file and suspend to collect on my record until he turns 70 early next year.

The SS agent is telling me we both have to be at FRA. I can't believe this as this scenario was recommended to us by Fido's SS experts. I don't want to leave $9K+ on the table.

HELP...is this true or do I need to talk to another agent?

I tried to do this online as well as apply for Part B Medicare for DH who is retiring in July, but their site isn't intuitive and we couldn't figure out how to do all this so am trying to make an appt.

The SS agent is telling me we both have to be at FRA. I can't believe this as this scenario was recommended to us by Fido's SS experts. I don't want to leave $9K+ on the table.

HELP...is this true or do I need to talk to another agent?

I tried to do this online as well as apply for Part B Medicare for DH who is retiring in July, but their site isn't intuitive and we couldn't figure out how to do all this so am trying to make an appt.