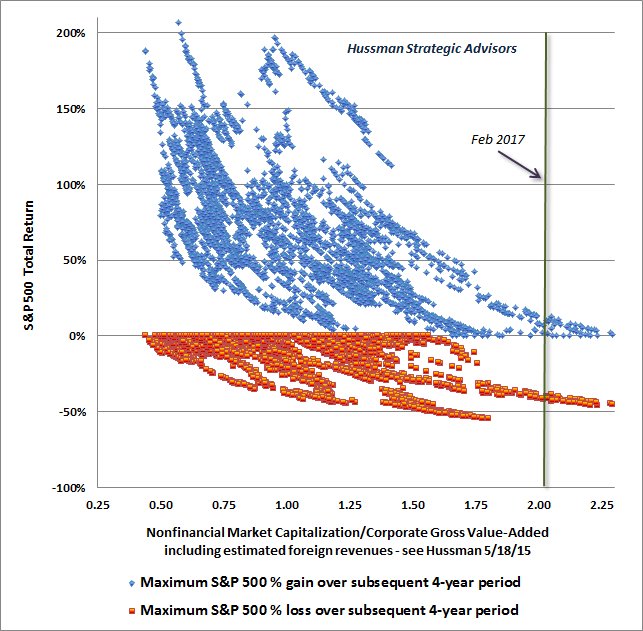

I like the depth of Hussman, learned a few things from his analysis. The big underlying problem (that he is aware of!) is trying to use statistics on the past to manage the future.

My own crash indicator is a fairly simple one: Equities are not worthwhile compared to bonds if in real terms the yield (CAPE) hits or drops below zero.

So if you have a CAPE of 25 = 4% and 4% inflation, trouble tends to happen very quickly and there is no harm being cautious. If the indicator goes positive again a few months in a row, get back in.

This happened only nine times since 1929, specifically:

- Late 2007 to late 2008: From 1500 to 900 (-40%)

- Late 2005 to late 2006 : From 1200 to 1300 (+8%)

- Mid 1999 late 2001: From 1300 to 1200 (-8%)

- Mid 1979 to early 1981: From 102 to 134 (+32%)

- Mid 1973 to late 1975: From 105 to 85 (-19%)

- Late 1968 to mid 1970: From 100 to 75 (-25%)

- Early 1951 to mid 1951: From 22 to 23 (+5%)

- Mid 1946 to late 1948: From 19 to 16 (-16%)

- Late 1941 to late 1942: from 10 to 9 (-10%)

That's the full list, no cheating

")

Three 'misfires' are in there, how bad are they?

- 2005: bonds were yielding 5%, so that's ok. Including dividends (2%) you missed out on 8%-5%+2% = a 5% run-up

- 1979: bonds at ~10%, so you got 15% from there. So you missed out on 32% - 15% + 5% div. = +22%. Ouch.

- 1951: bonds at 2.5%. Missed: 5% - 2.5% + 7% = +9.5%. Also ouch.

... and which big crashes did it miss (drops of more than 10% yoy)?

- Mid 1987 to early 1988: 330 to 270 (-20%)

- Early 1977 to early 1978: 104 to 90 (-14%)

- Late 1961 to late 1962: 72 to 60 (-17%)

- Early 1937 to mid 1938: 18 to 10 (-45%)

- ... and 1929 ...

So what, you say? Well, doing this consistently gets you fewer downdrafts with structural outperformance of ~3% per annum.

Will this work in the future? I don't know. What I do know is that right now the CAPE is approaching 30 and inflation is climbing above 2%. So I'm watching inflation numbers pretty closely.

[Note: numbers rounded, so don't shoot the pianist]