REWahoo

Give me a museum and I'll fill it. (Picasso) Give

55/30/15 baseball cards/beanie babies/tulip bulbs.

For safety I am gradually moving $$ into CDs from Stanford Intl Bank of Antigua.

At least you aren't a dirty market timer...

55/30/15 baseball cards/beanie babies/tulip bulbs.

For safety I am gradually moving $$ into CDs from Stanford Intl Bank of Antigua.

Did you get this info via web site or did one of the VG advisors gives you this info?

TJ

")

If you were a market timer you'd be buying whatever Winn-Dixie has on sale this week....40% Coors Light/40% Miller Lite/20% Corona

If you were a market timer you'd be buying whatever Winn-Dixie has on sale this week....

Did you get this info via web site or did one of the VG advisors gives you this info?

TJ

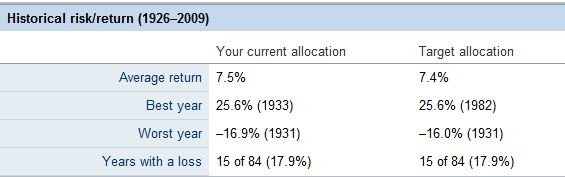

Alan, I like the VG portfolio watch of your allocation. Especially the only 17% down years.35% equities 65% bonds & cash

Welcome to the forum.

40/60 AA

Rationale: chicken feathers

Is everyone just using the fund description for their allocation or the actual holdings of their funds?

Marc