No doubt -- I think it would be more like sales taxes where food is exempt, and probably medicine as well. Though I would expect some social engineering over which foods are exempt, with those perceived as "unhealthy" being hit with a VAT.

There was a bit of fuss a year or 2 back when Pringles had VAT added to them in the UK. The government decided that the amount of potato in a Pringle had fallen below the threshold to class it as a food item

") (Pringles are now classed the same as potato crisps and lose some price advantage)

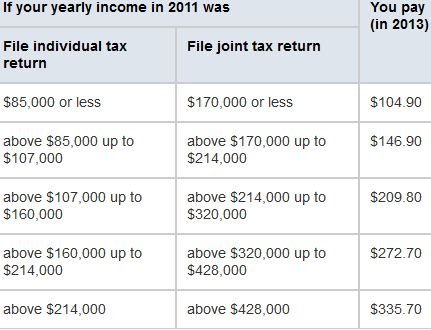

(Pringles are now classed the same as potato crisps and lose some price advantage)This table below is an example of what we would get to over here if VAT came to be, and food was excluded.

VFOOD8160 - Excepted items: snack products: examples of the VAT liability of common snack products

from the table, Pringles are subject to VAT, but Tortilla chips are not