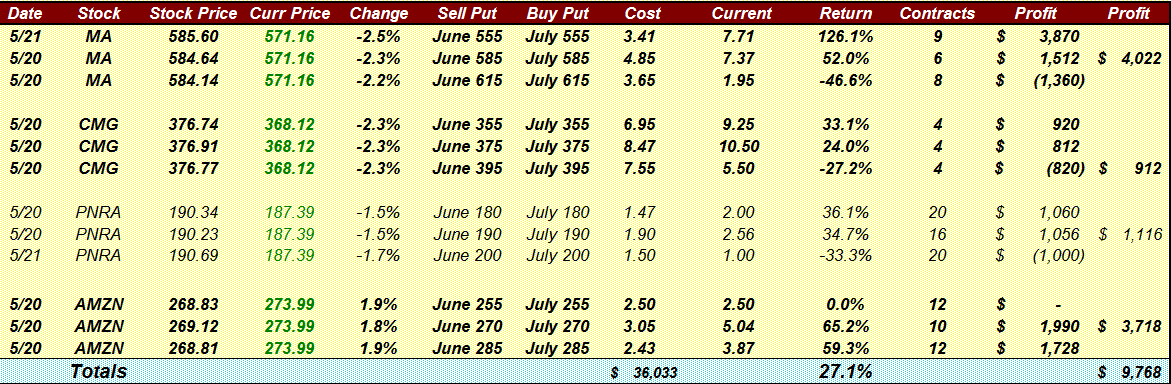

Since I got an email question on this subject, I thought I add a few more thoughts on risk and practicality.

If we look an aggressive retirement portfolio of ~$1 million, consisting of 5,000 SPY (~700K), 100K each in small cap, bonds, and international. Now compare this to the same portfolio in an IRA of ~700K cash but instead of holding 5,000 SPY we trade 50 SPY cash secured puts each week. I believe what utrecht is saying and both backtesting and common sense seem to bear out is that in an bull market this will lag B&H, but in a bear market it will outperform.

Overall this seem like Alpha for a retiree because what we are all struggling to do is capture the superior returns of stocks without having to suffer through their higher volatility as long as the total return is the same it is win as Utrecht says.

The other advantage of making these trades from an IRA is it is easier since you don't have to worry tax reporting and it is far more tax efficient than employing this strategy in taxable account (more on this latter).

But what I found out was from a practical point it was PITA to employ this strategy in a IRA. For example on Friday I sell 50 SPY puts @140, next Friday the SPY is at 141 but I can not write SPY 141 next Friday, because I'm short 140 puts and since I can use margin. So I can either buy the puts for a a penny or two in the last few minutes of trading, or wait until Monday to write the new puts. So now I have two days a week I need to watch the market and what if Monday are up days for the market? than I lose vs B&H.

Now lets go back and look at doing the same thing in taxable account. You have plenty of margin available to buy as many contracts as you want with your 700K in cash. But this is the problem all of the profits you generate is taxed a short term cap gains. In contrast if we look at the situation for a B&H investor his is a far more tax efficient strategy. In the last year the SPY has gone from 120 to 140 so the B&H would have 100K in unrealized capital gain. Dividends from the portfolio would about 17K and interest 3K. If his rebalancing date was in Aug. He could sell 200 SPY for $28,000 and would have long term cap gains tax of 45K and ordinary income of only 3,000, he spends 40K and reinvests the rest. I suspect that even if selling puts has a slightly higher total return (as opposed to even) the tax consequences would more than wipe it out.

Not surprisingly Utrecht figured out hey I can have my cake and eat it to. I can still have a portfolio of 5000 SPY etc. and I can also trade the 50 contracts every week, and incur no margin charges, sweet!. However, as Fire51 points out you are taking on more risk, maybe not twice the risk but holding both 5,000 SPY and being short 50 SPY put is significantly more risky than doing just one or the other. The reason it looks like gives superior return is because you are using leverage on an asset class which historically appreciates and incurring no penalty in the form of margin interest.

Overall this doesn't seem like an appropriate strategy for a retiree.

On the hand, in Bernstein latest ebook, The Age of Investor, he specifically recommends that young investor employ margin when they are in the early stages of investing. This seems like one of the least risky ways of doing it.

BTW, Utrecht not surprising we are both serious poker players...