bobebob

Dryer sheet wannabe

Greetings all,

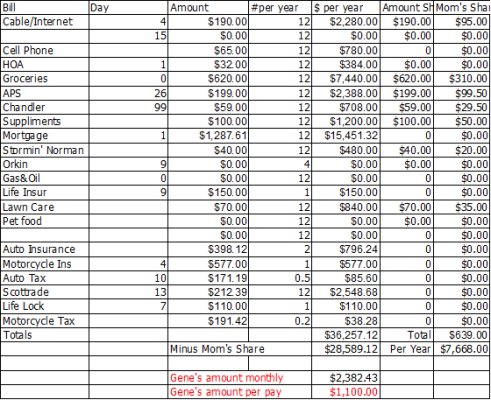

I have spent some time making up a financial spreadsheet to model my retirement.

https://www.amazon.com/clouddrive/share/FCpJZVXDjlNroGRotQMZj9HLd7RwDgfbHYk6z-c02Gc

I tried to factor everything into this (rather large) spreadsheet:

Taxes, Medicare, Medicare supplements, Medigap, healthcare coverage pre-Medicare, dental and vision, Social Security, using Roth IRA Contributions to cover budget expenses prior to age 59.5

Had to make some educated guesses here and there, but I think it’s pretty solid.

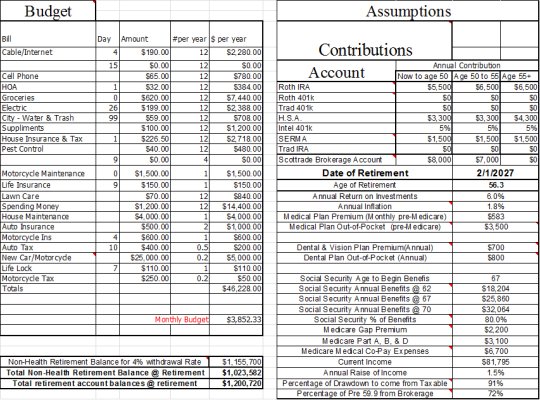

I tried to be reasonably pessimistic:

6% return on investments

1.8% inflation

Only getting 80% of the Social Security I should

No increases in SS

Maximum out-of-pocket costs for medical plan every year

Budget is pretty padded compared to how I live now. (no Fancy Feast for me)

Assuming there aren’t any horrific errors still in it, it shows me some interesting things:

1. The effect of a Health Savings Account on your medical expenses in retirement is HUGE. Especially if you retire early as it helps you cover the pre-Medicare years. By the time I need someone to take care of me, I should still be able to pay for long term care (or at least the premiums prior to needing it) out of my HSA even though I took out max out of pocket from it on my medical plans in my model.

2. In some scenarios, taking Social Security early actually increases your account balances in the long run. I think that is because you would be taking money out of investments to cover the period before you finally take SS and missing out on the interest that money would have made.

3. Having money in a brokerage account (or any non-retirement account) is vital if you want to retire before age 59.5 I found that I have a higher percentage of money in pre-tax accounts than I should. Had I started maxing out my Roth 401K earlier, I would have had more contributions I could have taken out to cover expenses before I reach the tax-haven age of 59.5

4. I will likely be able to retire earlier than I thought (age 56.3). I knocked about 2 ¾ years off my previous estimate (SWEET!). The only thing holding me back from retiring earlier than that is not having enough non-retirement funds available to cover those years before my retirement accounts can be tapped without penalty. If I waited until my original estimate of 58.5, the account values just get crazy. ( like 5 million at age 100)

5. I will be forking over more than half a million dollars to Uncle Sam during retirement. Yikes! Can I get my own Humvee?

If you have a few minutes, take a look at it and see if you can poke any holes in it. If you find any gross errors please let me know. I’ve played with it quite a bit and I think I’ve worked out most of the kinks, but I’m sure more will show up if you get creative.

I’ve played with it quite a bit and I think I’ve worked out most of the kinks, but I’m sure more will show up if you get creative.

Thanks for your time,

Gene

I have spent some time making up a financial spreadsheet to model my retirement.

https://www.amazon.com/clouddrive/share/FCpJZVXDjlNroGRotQMZj9HLd7RwDgfbHYk6z-c02Gc

I tried to factor everything into this (rather large) spreadsheet:

Taxes, Medicare, Medicare supplements, Medigap, healthcare coverage pre-Medicare, dental and vision, Social Security, using Roth IRA Contributions to cover budget expenses prior to age 59.5

Had to make some educated guesses here and there, but I think it’s pretty solid.

I tried to be reasonably pessimistic:

6% return on investments

1.8% inflation

Only getting 80% of the Social Security I should

No increases in SS

Maximum out-of-pocket costs for medical plan every year

Budget is pretty padded compared to how I live now. (no Fancy Feast for me)

Assuming there aren’t any horrific errors still in it, it shows me some interesting things:

1. The effect of a Health Savings Account on your medical expenses in retirement is HUGE. Especially if you retire early as it helps you cover the pre-Medicare years. By the time I need someone to take care of me, I should still be able to pay for long term care (or at least the premiums prior to needing it) out of my HSA even though I took out max out of pocket from it on my medical plans in my model.

2. In some scenarios, taking Social Security early actually increases your account balances in the long run. I think that is because you would be taking money out of investments to cover the period before you finally take SS and missing out on the interest that money would have made.

3. Having money in a brokerage account (or any non-retirement account) is vital if you want to retire before age 59.5 I found that I have a higher percentage of money in pre-tax accounts than I should. Had I started maxing out my Roth 401K earlier, I would have had more contributions I could have taken out to cover expenses before I reach the tax-haven age of 59.5

4. I will likely be able to retire earlier than I thought (age 56.3). I knocked about 2 ¾ years off my previous estimate (SWEET!). The only thing holding me back from retiring earlier than that is not having enough non-retirement funds available to cover those years before my retirement accounts can be tapped without penalty. If I waited until my original estimate of 58.5, the account values just get crazy. ( like 5 million at age 100)

5. I will be forking over more than half a million dollars to Uncle Sam during retirement. Yikes! Can I get my own Humvee?

If you have a few minutes, take a look at it and see if you can poke any holes in it. If you find any gross errors please let me know.

I’ve played with it quite a bit and I think I’ve worked out most of the kinks, but I’m sure more will show up if you get creative.Thanks for your time,

Gene