Ed B

Recycles dryer sheets

So I am 24 months out from RE if markets are kind to me. I will be 59 and DW will be 58. About 74% of retirement revenue before my SS is from non-COLA pension. I am currently saving 22% of income in 401K counting company match. I will have access to company retiree health and I will need to draw from my assets to bridge from ER to starting my SS. My wife is on SSDI and will be medicare eligible March 2018, so my health insurance needs will be for me and DW's supplemental coverage(s).

But one of my nagging concerns with our 401K is the horrible investment choices. The only ones that are Morning Star 4-star or better are an S&P 500 Indexed Equity Fund and our company stock which has done VERY well, but is very risky. The Target Date Funds are ranked 1-star and 2-star by Morning Star. The Index Bond fund has dropped from 4-star to 3-star and has been getting murdered for over a year. The various International Funds are bad, and even the TIPS fund and other "safe" funds other than Stable Value are bleeding money. I need some growth to reach my target by June 2019 but I also don't want to be so exposed to risk that I get destroyed by a 2008 type event in 2018 or 2019 leading up to ER.

So I finally signed up for the Self-Directed Brokerage Account option in our 401K plan which uses TD Ameritrade. After studying the Vanguard W's for several months for my Mother, I decided to use one of them as a defensive position that will still make "something", and put the rest in mostly equities to reach a ~60/40 AA. Even after reading a lot here, reading many artciles, running FireCalc & i-ORP over and over I am still definitely experiencing that tension between regret over missed opportunity and "Putting it all on Red".

Before setting up the SDBA I had re-balanced my funds to this for several months and was investing in Stable Value with 4% going into LMT each week.

S&P 500 - 25%

TD 2030 - 25%

Stable Value - 25%

LMT - 25%

After setting up the SDBA my allocation looks like this:

I have already learned that I have to look at funds like Wellesley totally differently. Its big increases will come quarterly and end of year so I need to get distracted and stop looking at it. But even at that, it is doing more than the Stable value fund did. The thing that convinced me on Wellesely as a defensive position is had I invested in 2007, reinvesting all dividends and CGs, I will have lost %% and recovered with a few % to the good in two years. Wellington was pretty good but not that good defensively. I compared several other high dividend MFs and ETFs and came away with Wellesley as a good choice for this investment tactic.

As you can see I did decide to "put some on red and let it spin" by investing in VGT and FTEC. The latter was leftover cash. I could get hurt here but I feel good about that the IT sector. And since they are ETF's, if things go bad I can decide to let it ride or sell quickly if I feel the need.

I left some money in the 401K's native S&P 500 Indexed fund. It is the one fund that doesn't suck aside from company stock. I also put 13% in High Yield Bonds in the native 401K (represented by Vanguard's symbol) but I am not crazy about that. And as you see I also have 13% in LMT. I sold half of it and moved those funds to the SDBA, but keeping even 13% in an individual equity is risky leading up to ER. But it has done so well that it could drop $15/share and I would still be thousands ahead. I will be watching it closely and monitoring POTUS tweets and the impact that may have, but as of this moment I am playing with house money with LMT.

I don't suppose I have a defined question, but I invite comments, warnings, and suggestions.

But one of my nagging concerns with our 401K is the horrible investment choices. The only ones that are Morning Star 4-star or better are an S&P 500 Indexed Equity Fund and our company stock which has done VERY well, but is very risky. The Target Date Funds are ranked 1-star and 2-star by Morning Star. The Index Bond fund has dropped from 4-star to 3-star and has been getting murdered for over a year. The various International Funds are bad, and even the TIPS fund and other "safe" funds other than Stable Value are bleeding money. I need some growth to reach my target by June 2019 but I also don't want to be so exposed to risk that I get destroyed by a 2008 type event in 2018 or 2019 leading up to ER.

So I finally signed up for the Self-Directed Brokerage Account option in our 401K plan which uses TD Ameritrade. After studying the Vanguard W's for several months for my Mother, I decided to use one of them as a defensive position that will still make "something", and put the rest in mostly equities to reach a ~60/40 AA. Even after reading a lot here, reading many artciles, running FireCalc & i-ORP over and over I am still definitely experiencing that tension between regret over missed opportunity and "Putting it all on Red".

Before setting up the SDBA I had re-balanced my funds to this for several months and was investing in Stable Value with 4% going into LMT each week.

S&P 500 - 25%

TD 2030 - 25%

Stable Value - 25%

LMT - 25%

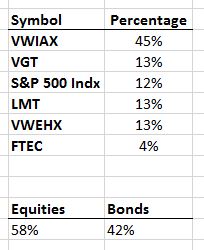

After setting up the SDBA my allocation looks like this:

I have already learned that I have to look at funds like Wellesley totally differently. Its big increases will come quarterly and end of year so I need to get distracted and stop looking at it. But even at that, it is doing more than the Stable value fund did. The thing that convinced me on Wellesely as a defensive position is had I invested in 2007, reinvesting all dividends and CGs, I will have lost %% and recovered with a few % to the good in two years. Wellington was pretty good but not that good defensively. I compared several other high dividend MFs and ETFs and came away with Wellesley as a good choice for this investment tactic.

As you can see I did decide to "put some on red and let it spin" by investing in VGT and FTEC. The latter was leftover cash. I could get hurt here but I feel good about that the IT sector. And since they are ETF's, if things go bad I can decide to let it ride or sell quickly if I feel the need.

I left some money in the 401K's native S&P 500 Indexed fund. It is the one fund that doesn't suck aside from company stock. I also put 13% in High Yield Bonds in the native 401K (represented by Vanguard's symbol) but I am not crazy about that. And as you see I also have 13% in LMT. I sold half of it and moved those funds to the SDBA, but keeping even 13% in an individual equity is risky leading up to ER. But it has done so well that it could drop $15/share and I would still be thousands ahead. I will be watching it closely and monitoring POTUS tweets and the impact that may have, but as of this moment I am playing with house money with LMT.

I don't suppose I have a defined question, but I invite comments, warnings, and suggestions.