Except you really can make 6%-7% or more if you venture into investment grade bonds.

thats def more enticing

as you know I'm not a bond guy

how far out do you have to go for that?

Except you really can make 6%-7% or more if you venture into investment grade bonds.

thats def more enticing

as you know I'm not a bond guy

how far out do you have to go for that?

I just bought some 9- 11 month ones in the 6.5%-7.2% range. You can buy non callables easily around 6% for longer duration.

There are a few ways to look at this. If we maintain 5% ROI, stay in the 12% tax bracket, 3% inflation with our SS we have 100% success with some left over after 30 years. That gives us $140k safe spending constant every year. We do not spend that much, but I’m thinking nursing home or independent living for one of us at some point. Even if one of us dies, the SS reduces, we’re ok. Or we get the 25% haircut, still ok. This stuff gets complicated and I’m using every calculator I can get my hands on

For those thinking we are near the top in terms of LT yields, you can pick up the US Treasury 30 year bond 1.25% coupon maturing 5/15/2050, issued 5/15/2020 for less than 50 cents on the dollar. (It reached a low today of 48 and 23/32nds and had a high over 101 in Aug 2020.) YTM is over 4.6%.

So much for a "risk free" investment (that is trading for less than half its original value, and for all those "well it will be redeemed at par" folks well I just lol.)

Yes. The problem with corporates, for most of us anyway, is that we don't have enough time or money to build a reasonably diversified portfolio.wow

thats pretty good

Yes, but it's all relative. Today, buying a 5 year CD Ladder thats averaging ~ 5% is priced that high due to inflation running at like 3.25% so yeah you can make 1.75% adjusted for 5 years. Maybe a little higher if you shop around I would imagine. Again, its a way to mitigate volatility. Not to get some great return on your money.

Yes. The problem with corporates, for most of us anyway, is that we don't have enough time or money to build a reasonably diversified portfolio.

I am on the investment committee of a small nonprofit. On the FI side we have 2-3 $million in corporates because our strict instruction to the FA is to stay out of bond funds. He has built the portfolio using $10K purchases of investment grade bonds, resulting in over 100 positions. Too many issues, IMO, for an amateur to select and monitor effectively. This assumes that you have 7 figures to put into bonds in the first place.

The problem with corporates, for most of us anyway, is that we don't have enough time or money to build a reasonably diversified portfolio.

I don't get why people get excited about being able to get higher rates on treasuries and CDS. Sure, rates are higher, but that's just in response to higher inflation. The only reason I would include such securities in my portfolio would be to mitigate volatility of the stock market.

I don't get why people get excited about being able to get higher rates on treasuries and CDS. Sure, rates are higher, but that's just in response to higher inflation. The only reason I would include such securities in my portfolio would be to mitigate volatility of the stock market.

I don't get why people get excited about being able to get higher rates on treasuries and CDS. Sure, rates are higher, but that's just in response to higher inflation. The only reason I would include such securities in my portfolio would be to mitigate volatility of the stock market.

Question: is it better to take cash for dividends and use it to rebalance, or buy high yield CD’s, or auto reinvest?

Other info: My IRA equity portfolio is in 3 US, low cost, broad market ETFs. They generate between $37k -$41k/ year in dividends, set to automatically reinvest. Am several years out from RMDs, maintaining 5 years of fixed, annual 4% WD’s.

Stay the course? Take a more active role in managing dividends?

Appreciate any thoughts/ideas.

... Appreciate any thoughts/ideas.

As you imply I would say that maximum position sizes should primarily be driven by the overall size of the portfolio. A $10K maximum in a $20K portfolio would be silly, but in a $2M it's less than 1%. For our FA its not the burden that it would be for a DIY-er because he is researching and buying for a number of portfolios. A $25K maximum, though, certainly means less work for a DIY-er and if it works for you that's all that matters.I would say that a maximum of $10k per credit for a $2-3m corporate bond portfolio is pretty low. I limit any one corporate bond credit to $25k, but I also generally only invest in A or better, so a little north of the bottom of investment grade credits. ...

Yeah. At every one of our quarterly reviews we look at the spreads and trends. As a result of weak spreads from time to time, we do have some govvies in the portfolio.Recently, the premium of corporates over similar term agency bonds or even brokered CDs isn't enough to be attractive to me, but there are occasional exceptions.

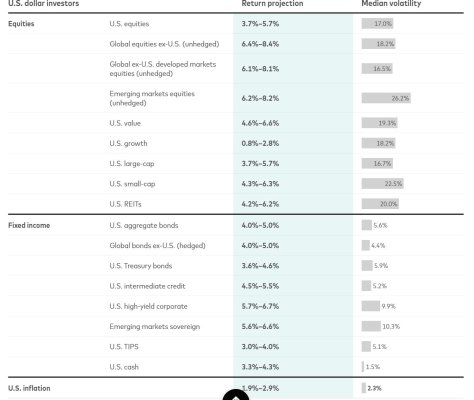

Vanguard forecasts that the total return for US equities for the next decade will be 3.7-5.7% with 17.0% median volatility and the total return for US aggregate bonds will be 4.0-5.0% with 5.6% median volatility... so if they are right, given the similarity in returns why assume the significanty different volatility?

That said, nobody knows nuttin.

https://corporate.vanguard.com/cont.../investment-economic-outlook-august-2023.html

...Be curious what they were saying back in 1963, 1973, 1983, 1993, 2003 and 2013. ....

I'm slowly recovering as my shorter term CD's mature and I'm moving that money into SWVXX (which pays over 5% and can be turned into cash, penalty free, in one day.) You know, you just can't fix stupid!

I'm slowly recovering as my shorter term CD's mature and I'm moving that money into SWVXX (which pays over 5% and can be turned into cash, penalty free, in one day.) You know, you just can't fix stupid!COcheesehead is right - duration kills. Or can kill.

I don't remember who said this (it was a big name in the financial world) [paraphrasing since I don't have the original source] - The difference between 30-year and 1-year yields is less than 1%. That's not an investment decision, that's an intelligence test.

Low rates and low delta rates between long and short bonds strongly suggest pulling back on duration. In a balanced portfolio, FI is primarily for volatility dampening, so you can rebalance when stocks take a nosedive and you buy them on sale. For those already retired, without outside income sources, volatility is more important.

Question: is it better to take cash for dividends and use it to rebalance, or buy high yield CD’s, or auto reinvest?

Other info: My IRA equity portfolio is in 3 US, low cost, broad market ETFs. They generate between $37k -$41k/ year in dividends, set to automatically reinvest. Am several years out from RMDs, maintaining 5 years of fixed, annual 4% WD’s.

Stay the course? Take a more active role in managing dividends?

Appreciate any thoughts/ideas.

No.

IMO the market is still the best place to stay invested. CDs are short lived compared to gains in the market for the long haul.

Getting out, getting in, isn't for me and from experience it never has worked out for me.

I plan to stay in that 80/20AA till my last breath and just let it ride the times.

We’re thinking of selling some our stock index funds to buy safe long-term bonds.

We’ll be 66 next year.