I mentioned last fall because my balance plunged and I lived with regret for the next several months, wishing I had listened to myself when I thought I shouldn't be so risky this close to retirement. I don't want to have to go through that again if I don't have to. ...

^This is your answer right here.

If market turbulence makes you air sick, you've got too much in the market.

For me, 2018 was great as my highly conservative allocation ended up being one of the higher year end performers when the market flew into the late 2018 air pocket... Its all about what lets you sleep at night.

I'm the odd duck on this board in that I am mostly in cash (CDs and a Stable Value Fund in the 401K). I've got about as much in gold as I have in stocks. But before you go there:

a) as others have suggested, make sure you've run firecalc or whatever tool with the higher cash balance (lower projected returns) vs. the tool default asset allocation returns.

b) factor in inflation, especially health care/LTC

c) allot for some surprise expenditures/income hits... replace a car, a HVAC, a SS haircut, etc.

If after doing that you're still comfortable with the lower returns of a conservative AA, there is nothing wrong with "if you've won the game, quit playing" and move to a more conservative allocation.

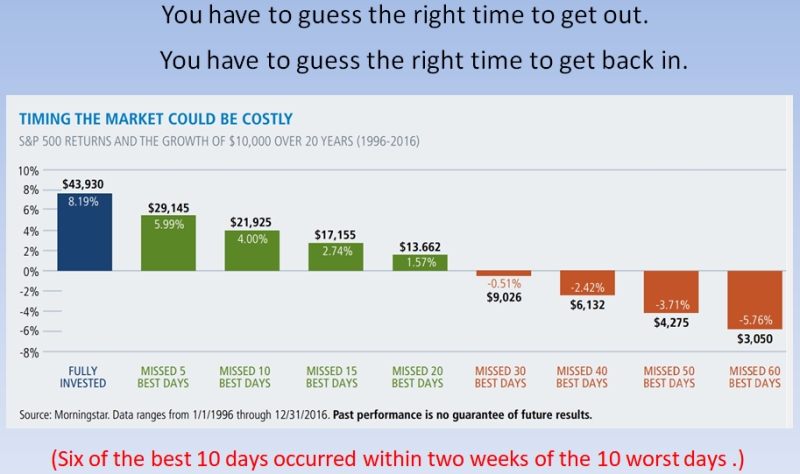

As far as going to cash temporarily on the way to a different asset mix, you gotta ask why... Waiting for a crash first? Crashes now days are flash crashes... the printing presses fire up and the market is up again before you fully absorb it was down... (until that one time it doesn't but then you'll wish you had rice and beans vs. cash)

Just round the corner to whatever you want your long term AA to be and shuffle the piles until you're there.

")