What tools do you use to estimate the time it'll take you to FIRE? I've seen some online calculators but they are a little underwhelming (i.e. Networthify).

They assume a fixed return on investment and no asset allocation.

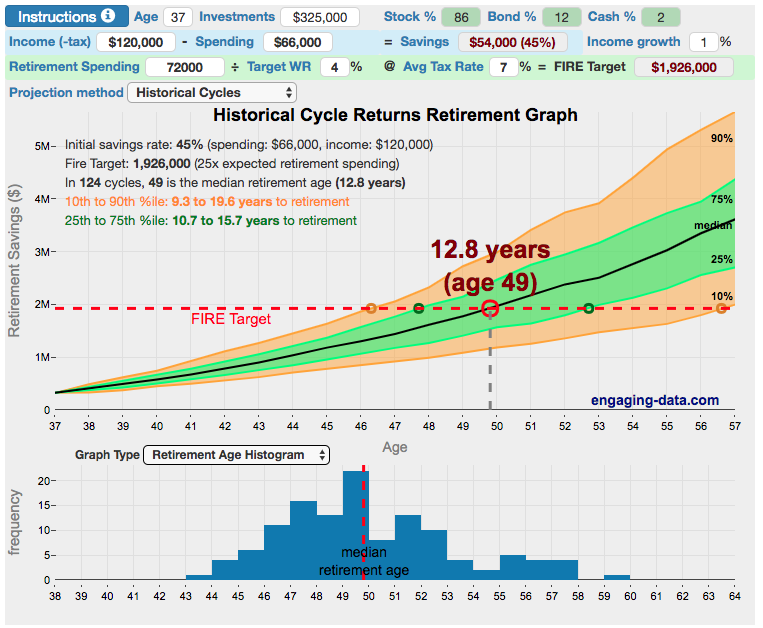

FIRECalc would be interesting to use given all the data embedded within, but it doesn't seem to be able to run in "when will I hit my magic number?" mode.

Does anyone have a go-to tool they use for projecting when they'll be able to pull the plug?

They assume a fixed return on investment and no asset allocation.

FIRECalc would be interesting to use given all the data embedded within, but it doesn't seem to be able to run in "when will I hit my magic number?" mode.

Does anyone have a go-to tool they use for projecting when they'll be able to pull the plug?

Technical error I am sure.

Technical error I am sure.") ) It wasn't that hard back in the early days since I knew FIRE was a very long ways out and the numbers were a lot smaller. About the time I reached ~50 years of age, things started to take shape both in my mind and on my evolving custom spreadsheets. It was about then that I started getting serious about tracking things. Everything was done on spreadsheets and I felt very comfortable with what was going into the spreadsheets, the "assumptions" that were made (e.g. inflation rates) life expectancy, return rates, tax rates, RMD's, etc, etc.

) It wasn't that hard back in the early days since I knew FIRE was a very long ways out and the numbers were a lot smaller. About the time I reached ~50 years of age, things started to take shape both in my mind and on my evolving custom spreadsheets. It was about then that I started getting serious about tracking things. Everything was done on spreadsheets and I felt very comfortable with what was going into the spreadsheets, the "assumptions" that were made (e.g. inflation rates) life expectancy, return rates, tax rates, RMD's, etc, etc.