pb4uski

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

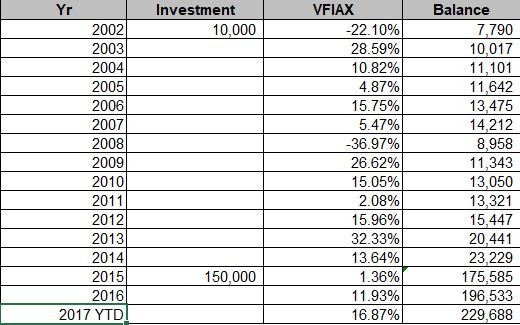

Here is what my most current info states on this Annuity.

Variable Annuity

Non Pension Annuity

Min Guarantee Interest 3.50%

Cash/Accumulated Value $213,006.12

Surrender Charge $0.00

Cash Surrender Value $213, 006.12

Cost basis $160,000.00

Taxable Gain $53,006.12

Usually a variable annuity doesn't have a minimum guaranteed interest rate, unless perhaps that 3.5% relates to the general account option within the VA.

How long have you had this annuity? did you make a single premium payment or have you made monthly or yearly payments? Given the cost basis is a nice round number I'm suspecting that it was a single premium.

Usually a variable annuity has different "subaccounts" that the money is invested in or a "general account" option where it is invested in the insurer's general account. What is your annuity invested in? It should say on your statement.

I'm generally not keen on variable annuities, but if this one has a 3.5% minimum guarantee, that may be something valuable that you can't get today that you can take advantage of.

However, I wouldn't be adding more money to it until you have a clear understanding of it.

Do you own this variable annuity directly or is it in an IRA?

Last edited: