I have had our money money in mutual funds since the late 80s. I have a paid for house, a $250k piece of land that is now for sale and a few other minor assets besides the Mutual fund / ETF portfolio.

At 68 I'm now starting to rethink my asset allocation. It was a great ride 2009 thru 2021. But not as much fun the last couple years. I went through 2001 and 2008 and not all that spooked by this, but at 68 starting to wonder if I should change my AA. We have been in spend down for 5 years, soon we will start SS. This will bring our withdrawal rate to 1% or under. I am mostly investing for my kids future as I feel we have more than enough, even if we had a 50% market plunge. After 5 years of withdrawals our balance is higher then 5 years ago.

We have $1.8M in a mix of mutual funds under SEPS, IRAs, Roths, HSAs and taxable accounts. Of that, about $300k is in high yield MM accounts, $200k after a Roth conversion, I wasn't sure I wanted in the market yet, and $100k in various accounts in MMs, mostly because of lack of action.

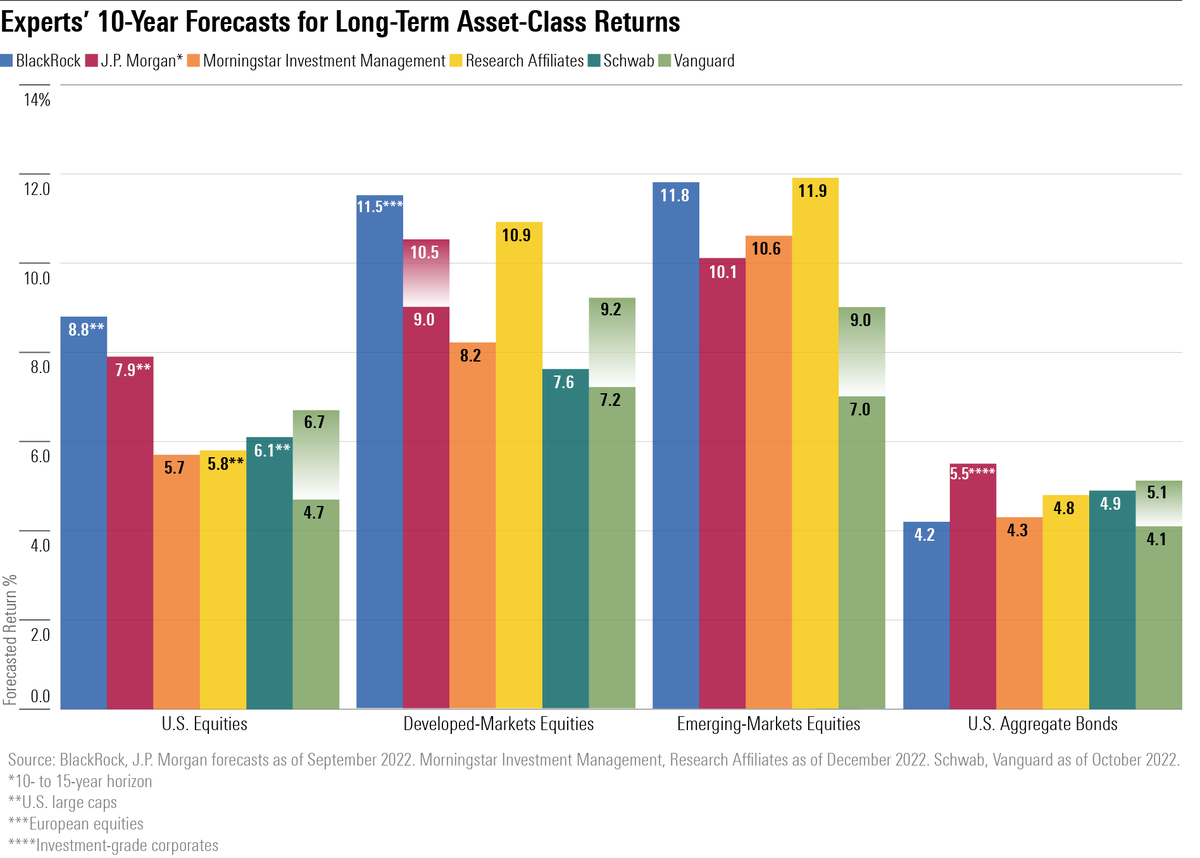

I'm leery of bond funds, because IF rates have peaked and do start to fall so will the bond funds. (I have a friend whose portfolio kept dropping as interest rates rose.) So individual bonds would be my choice as I can hold until maturity, but I have never bought a bond, or a CD or a TIP or any fixed income investment. That leaves me lost as to what to do or how to do it and if I should do it. I'm mostly in Vanguard but have an IBKR and a an HSA in Fidelity. I know this is a personal opinion, as there are investors with 100% equities and those with a mix of equities and bonds.

I'd like your comments.

At 68 I'm now starting to rethink my asset allocation. It was a great ride 2009 thru 2021. But not as much fun the last couple years. I went through 2001 and 2008 and not all that spooked by this, but at 68 starting to wonder if I should change my AA. We have been in spend down for 5 years, soon we will start SS. This will bring our withdrawal rate to 1% or under. I am mostly investing for my kids future as I feel we have more than enough, even if we had a 50% market plunge. After 5 years of withdrawals our balance is higher then 5 years ago.

We have $1.8M in a mix of mutual funds under SEPS, IRAs, Roths, HSAs and taxable accounts. Of that, about $300k is in high yield MM accounts, $200k after a Roth conversion, I wasn't sure I wanted in the market yet, and $100k in various accounts in MMs, mostly because of lack of action.

I'm leery of bond funds, because IF rates have peaked and do start to fall so will the bond funds. (I have a friend whose portfolio kept dropping as interest rates rose.) So individual bonds would be my choice as I can hold until maturity, but I have never bought a bond, or a CD or a TIP or any fixed income investment. That leaves me lost as to what to do or how to do it and if I should do it. I'm mostly in Vanguard but have an IBKR and a an HSA in Fidelity. I know this is a personal opinion, as there are investors with 100% equities and those with a mix of equities and bonds.

I'd like your comments.

") .That would be different if the market was down 50%. I'd still sleep, but I'd be kicking myself all the way to the bed.

.That would be different if the market was down 50%. I'd still sleep, but I'd be kicking myself all the way to the bed.