Hi, I'm new here after being referred on another website for some help on the ACA. I got a lot of great info, so I'm hoping for a sanity check on our particular situation.

Our general situation is that we are 56 and 57 and retired last year. My wife has a small pension and very low earned income from sporadic work. We are targeting an annual budget of around $100k. We have significant Trad IRA, LTCG assets, some Roth, and some HSA dollars available. I estimate we can cover our expenses for the next 4-5 years via LTCG, Roth and HSA. This will still leave about 5 years until we are eligible for Medicare.

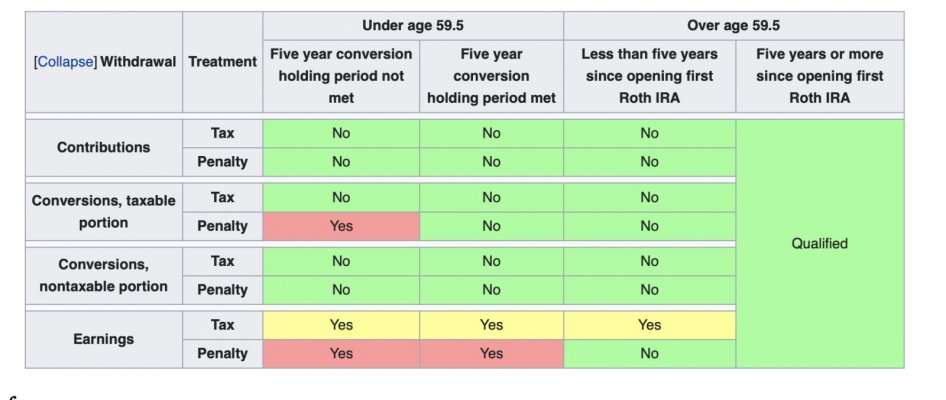

This tax year our funding so far as been largely cash on hand. This would easily allow us to keep our taxable income to the $89250 0% cap gains threshold. We will still qualify for a very nice ACA subsidy. My plan is sell as much of the LTCG assets this year as possible to stay below the threshold to fund the last part of the year and reset the basis. Possibly repeat this next year depending on the amount of cap gains left, and then do a Roth recharacterization on anything left up to the limit. Once all the cap gains are taken at 0%, continue to do Roth recharacterizations at least up to the 12% limit.

The downside is that we will run-out of tax-free money before age 65, but I'm not sure if we want to do Roth recharacterization at a higher tax rate. If the ACA cliff returns in 2026 we will lose over $10k in subsidy, so it might make sense, but with this plan the earliest we would have that recharacterized Roth available is nearly at Medicare time. Alternatively, I think we could do much higher recharacterizations for the next 5 years at the expense of paying capital gains and higher taxes, but we would still lose the subsidy for a couple of years.

I've been looking for a CPA with expertise in retirement, but haven't found any in my area accepting new clients. I've tried some of the online calculators, but they seem to be focused on RMD tax impacts and it seems like it would best for us to wait until 65 to more aggressively convert based on the current ACA subsidy. I hoping folks who have gone through this type of scenario could provide their insight and any critical elements I'm missing. Thanks.

Our general situation is that we are 56 and 57 and retired last year. My wife has a small pension and very low earned income from sporadic work. We are targeting an annual budget of around $100k. We have significant Trad IRA, LTCG assets, some Roth, and some HSA dollars available. I estimate we can cover our expenses for the next 4-5 years via LTCG, Roth and HSA. This will still leave about 5 years until we are eligible for Medicare.

This tax year our funding so far as been largely cash on hand. This would easily allow us to keep our taxable income to the $89250 0% cap gains threshold. We will still qualify for a very nice ACA subsidy. My plan is sell as much of the LTCG assets this year as possible to stay below the threshold to fund the last part of the year and reset the basis. Possibly repeat this next year depending on the amount of cap gains left, and then do a Roth recharacterization on anything left up to the limit. Once all the cap gains are taken at 0%, continue to do Roth recharacterizations at least up to the 12% limit.

The downside is that we will run-out of tax-free money before age 65, but I'm not sure if we want to do Roth recharacterization at a higher tax rate. If the ACA cliff returns in 2026 we will lose over $10k in subsidy, so it might make sense, but with this plan the earliest we would have that recharacterized Roth available is nearly at Medicare time. Alternatively, I think we could do much higher recharacterizations for the next 5 years at the expense of paying capital gains and higher taxes, but we would still lose the subsidy for a couple of years.

I've been looking for a CPA with expertise in retirement, but haven't found any in my area accepting new clients. I've tried some of the online calculators, but they seem to be focused on RMD tax impacts and it seems like it would best for us to wait until 65 to more aggressively convert based on the current ACA subsidy. I hoping folks who have gone through this type of scenario could provide their insight and any critical elements I'm missing. Thanks.