It's like rolling dice or flipping coins. There is always the probability of a long streak of one result, but the longer you go the less likely that the streak will be unbroken.

In the book

The Only Investment Guide You Will Ever Need the author tells the story of lining up 256 people, giving them a fair coin, and asking them to flip heads 8 times in a row. Amazingly, one guy did it! What skill! What concentration! What courage! No.... What nonsense!!!!!!! Even worse is the assumption that since Mr. Jones managed to flip heads eight times in a row, he is more likely to do it again than the others.

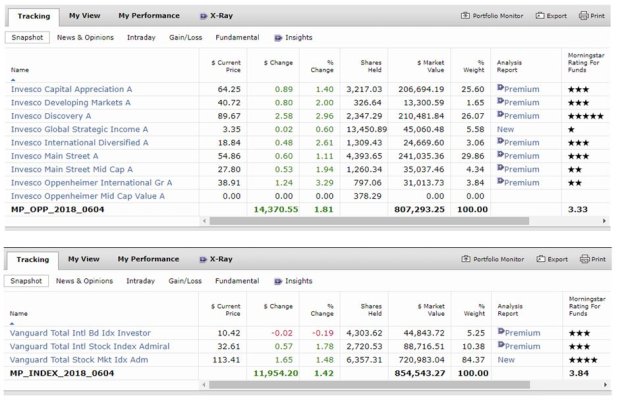

The only guy I ever invested with who seemed to consistently beat the average fund was a fellow named Micheal Price who ran a fund called Mutual Shares. The fund invested in distressed and bankrupt companies. It did great. I sold after Mutual Shares was bought by another fund outfit.

Unfortunately, Mr. Price died about two weeks ago.

https://www.bloombergquint.com/markets/michael-price-who-saw-value-in-companies-struggles-dies-at-70

He searched for value amid beaten-down companies. “We like to buy a security only if we think it is selling for at least 25% less than its market value,” he told Fortune magazine for a

1996 profile.

“When a company gets into trouble and starts to miss its earnings, analysts drop coverage because they don’t want to embarrass their firm with bad calls,” he told Fortune. “So mainstream Wall Street isn’t looking anymore. Which pond would you rather fish in, one with a lot of fishermen or only a few?”

He searched for value amid beaten-down companies. “We like to buy a security only if we think it is selling for at least 25% less than its market value,” he told Fortune magazine for a 1996 profile. “When a company gets into trouble and starts to miss its earnings, analysts drop coverage because they don’t want to embarrass their firm with bad calls,” he told Fortune. “So mainstream Wall Street

Read more at:

https://www.bloombergquint.com/markets/michael-price-who-saw-value-in-companies-struggles-dies-at-70

Copyright © BloombergQuint

He searched for value amid beaten-down companies. “We like to buy a security only if we think it is selling for at least 25% less than its market value,” he told Fortune magazine for a 1996 profile. “When a company gets into trouble and starts to miss its earnings, analysts drop coverage because they don’t want to embarrass their firm with bad calls,” he told Fortune. “So mainstream Wall Street

Read more at:

https://www.bloombergquint.com/markets/michael-price-who-saw-value-in-companies-struggles-dies-at-70

Copyright © BloombergQuint

He searched for value amid beaten-down companies. “We like to buy a security only if we think it is selling for at least 25% less than its market value,” he told Fortune magazine for a 1996 profile. “When a company gets into trouble and starts to miss its earnings, analysts drop coverage because they don’t want to embarrass their firm with bad calls,” he told Fortune. “So mainstream Wall Street

Read more at:

https://www.bloombergquint.com/markets/michael-price-who-saw-value-in-companies-struggles-dies-at-70

Copyright © BloombergQuint