It is a tough choice and a lot of people disagree on where the market is heading.

Personally, my PhD was in Immunology studying non-linear non-parametric data and I was forced to develop my own set of equations to analyze experimental data. The other 2 areas that perform the same types of analysis are 1) the weather and 2) the stock market. I diverge from the subject to explain how my sense of what is "normal" and what is not is defined by my professional history. When I was doing my PhD at an Ivy League school I went to the Statistics Department to discuss my problems analyzing my data (fever measured by surgically implanted data loggers in dogs following tick bites with Lyme disease) and encountered a weird thing. All the people with PhD's in this area had left academia and were all working in Wall Street hence why I had to develop new and innovative ways to analyze this kind of data which resulted in my obtaining my PhD. At the time I wasn't interested whatsoever in the stock market (or the weather although I am a commercial pilot) but rather in analyzing pathogenesis in animals exposed to high-consequence pathogens.

My point is that when I married my third wife who is in the stock market as a Day Trader (quite successful by the way) I took it upon myself to model the market data to help her. She has a PhD in Physics so quite capable on her own and I am a dilatant in this area. Interestingly, I found the stock market to be completely unnatural and not follow any predictable models meaning it is completely manipulated thus incapable of modeling unless you know the exact decision process that the manipulators are using. This is my area and I know what I am talking about. However, knowing this also lets you piggyback on the bog boy traders such as market makers, etc., and cheat as they do. My wife focuses on specific stocks and follows the trades in finite detail and gets out early settling on roughly 1-2% gains every time. This is because it is impossible to know when they have gained enough and get out quick. They are using algorithmic trading which operates beneath the normal system and far faster than any human can. Anyway, after small gains, we get out and then look for the next opportunity. Rinse and repeat. The goal is roughly $1,000 a day and call it quits for the day. Usually, this is a couple of hours. Sometimes we have gotten trapped and have to wait it out and a couple of times it was months. But, we never trade with more than 30% of assets so can handle small losses. This has been successful but we also see enormous chaos and when it begins and go to 100% cash. We did this in January 2020 and again in February 2022. We haven't lost a cent since but did miss out on some wild swings and some obvious gains. However, the risk is very high now.

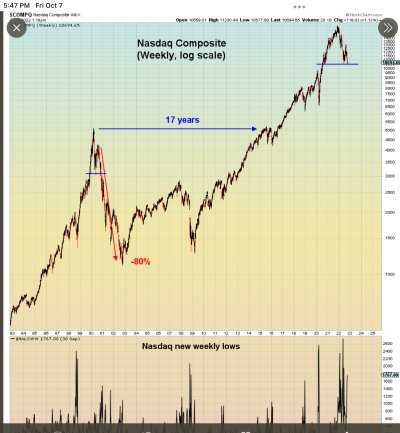

What I have realized is the massive manipulation and cheating on the markets is sustained by the US debt which is massively out of control. The DOW, as an example, is way above where it would naturally be and as the capitalistic system demands a correction MUST occur. There is a huge disparity in the economy supported only by continued infusions of fiat money which has in the past been sustained by the reserve currency status. These days are slowly disappearing due to actions by the US government which impacts foreign currency transactions that are slowly moving away from trades in dollars and even using the SWIFT system altogether. Capitalistic systems need corrections which roughly occur every 7 years. Actions by the Fed (pumping in huge amounts) have interceded on these corrections which now have been circumvented twice. The corrections must occur to return the system to a sort of stability so now we have 3 corrections coming, the first 2 which were circumvented and the third that needs to happen now. The DOW needs to return to its natural place which is roughly 18,000. Yes, the Fed will intervene again but every time it happens the pain will be worse further down the line. The dollar is still being used as a reserve currency and there is perhaps enough use to still support it a third time. However, some unpredictable (by us) black swan event like China dumping their dollars, blowing up the Turkish stream pipeline, nuclear war, etc. will cause a major swing away from the dollar if the US is perceived to be the culprit and thus unreliable. The de-dollarization is happening slowly anyway but this would accelerate it perhaps dramatically. No one outside the US wanted this to happen but here we are. What happens next is the big question.

My point to all of this is betting on US equities is a very risky thing now. So, diversification is the key. Land, gold, diamonds, US equities, and foreign equities, are a smart move but not very liquid and perhaps not liquid enough to provide an income. We are sitting on a ton of cash, have land, and no equities so are equally exposed. My wife is resistant to moving assets into things she has no experience working with so we are hopeful things will stabilize and the dollar remains strong. I am less confident but we are also old now so for us it really is a matter of making it another 10 or so years and we have plenty of cash to live on and a large place to live on which I am now making off the grid completely.

A serious change to the US political system could make a huge difference and restore confidence in the dollar. Until then I am very concerned about where we are headed.