Ronnieboy

Full time employment: Posting here.

- Joined

- Feb 14, 2008

- Messages

- 748

Thanks everyone for the thoughtful and insightful replies!

Senator's comments and well thought-out portfolio remind me of other savvy posters at Bogleheads who've pointed out that Wellesley really doesn't have a "secret sauce" and that these days one can pretty much duplicate its performance with a 65:35 large cap value: IT corp. bond ETF approach. I would still choose Wellesley myself, but agree wholeheartedly that it'd be foolish to make such a concentrated portfolio one's whole enchilada. And of course it has no place in a taxable account. I will probably put my IRA (26% of total assets) in it and leave the rest in the Bogleheads 3 fund portfolio (though I have long since substituted Admiral shares of IT Treasury for Total Bond due to consistently better performance, benefitting from flight-to-safety [as we saw big-time this past week] and no state or local taxes]).

I love Paul Merman's generosity and overall investing savvy, but I've run the numbers on his "Ultimate Buy and Hold" and it has yielded around 5% during the entire time I've been ER'd. Other DFA slice-and-dice portfolios (check out Scott Burn's numbers over at AssetBuilder.com) are in the 3-3.5% range over the past 15 years - out of which you have to pay 1% portfolio mgmt/DFA access fees and the costs of a boatload of trades to keep the intricate slices balanced.

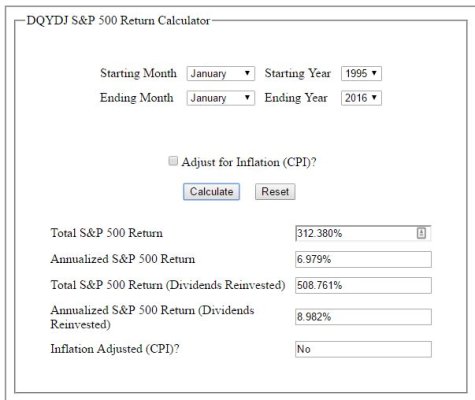

John Greaney, probably the earliest (and still one of the sharpest and most irreverent) ER site founders, has a great updated article on real world retiree returns on his site:

2015 Update: Real-Life Retiree Investment Returns

One of the portfolios he backtests is a William Bernstein MPT slice-and-dice, and Greaney's comment says it all, IMHO:

"While the MPT portfolio value has trailed the simple S&P500/fixed income portfolio (No. 1 above) by 21% as of Dec 31, 2015, advocates of this approach like its reduced volatility and sterling academic recommendations. Which brings us to an important investing truism -- it's OK to under perform as long as you're pleased with the results and proud of what you are doing."

Thanks again to everyone for sharing your thoughts. I learn a lot from this forum and am grateful to all of you.

I checked out Greaney's site and it looks like the Buffett portfolio is the way to go in both scenarios

") The WB portfolio is: 75% Stock/25% Fixed Income, rebalanced annually consisting of:75% BRKa 21% VFSTX, 4% VMMXX

The WB portfolio is: 75% Stock/25% Fixed Income, rebalanced annually consisting of:75% BRKa 21% VFSTX, 4% VMMXXIt has most success over both periods, 1994 to 2016 and 1999 to 2016.