street

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Nov 30, 2016

- Messages

- 9,539

Some interesting stuff and you guys are way above my head. LOL Thanks

+15.2 on 6/7, what a difference a week makes!

That was quick NYEXPAT.

For the folks who have CD's - do you factor in the interest on an accrual basis or a cash basis for investment performance?

That was quick NYEXPAT.

For the folks who have CD's - do you factor in the interest on an accrual basis or a cash basis for investment performance?

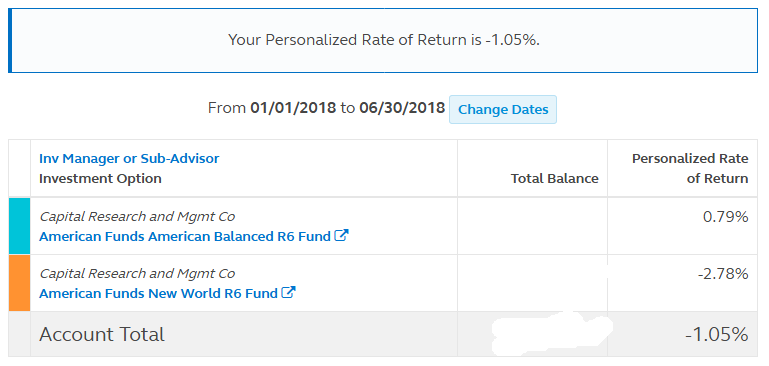

Thanks. Only up +0.50% YTD. Bond funds and Int'l equities dragging me down.+4.47 YTD

Regular bond interest is on an accrual basis. Baby bond and notes that pay monthly and quarterly are on a cash basis.

That was quick NYEXPAT.

For the folks who have CD's - do you factor in the interest on an accrual basis or a cash basis for investment performance?

YTD (June 30, 2018)

0.06% VTWNX Vg Target Retirement 2020 (54/46)*

*Looks like this one is now too far from 60/40 so should be dropped from this comparison.

Up 1.3%. Spent about 1% of that for 2018 budget hitherto. But the house value went up here in Bay Area, CA. I don't feel richer though.

.Your plan is interesting to me. I wonder if it would make for a good discussion in a separate thread? I have a similar thought process for bridging to the start of SoSec but I don't want to hijack this thread more than I just did. Thanks for sharing.FIDO – 4.33% YTD not including contributions. Balance has passed the January high.

Cash Balance Pension – 2% not including contributions.

A funny thing happened on the way to the forum this quarter; I discovered my true tolerance to risk.

After last year’s 24.5% run up in the 401k, realized that I could retire in two years at 59 instead of waiting until 60 – which is certainly not RE by many on this forum. (We are FI now but wanting to feather the nest a bit.) Original plan was to stay 100% invested until 2019, and then crawl into the bond tent to minimize SORR.

However, a corresponding 24.5% drop in my all equities FIDO account this year would be a real setback on the eve of FIRE causing me to work past 60. DW said do what makes you comfortable. So, in early April I pulled all of the EuroPac and ExUSA funds out and parked them in a MM account. This amount equaled projected SS gap income until FRA. As soon as I hit the ‘confirm’ for this transaction an unexpected wave of relief washed over me. Selected EuroPac and ExUSA because the dollar was gaining momentum (Lucky DMT that I am). Selected a MM account because the bond funds offered by my 401k are all in decline while the Fed normalizes rates. Went from looking at Fidelity once a day to once a week. Thought it was fun to watch the account grow – but apparently there was also a bit of unrecognized stress from risk taking.

First week of June decided to fully implement preFIRE portfolio and go to a 60/0/40 mix after subtracting the SS gap fund. Because of all the trade talk, kept the home boys fund of Russell2000. Sold all of the S&P500 and Russell3000 and stuffed that into the mattress. Immediately both of those indices went up 2%, so that move did not feel as smart in the following days – although the market has since taken back those gains.

My approach to retirement has been unorthodox with the experts claiming to start a bond glide path much earlier than this, instead of less than 2 years before retirement. (BTW – they are right and I am a lucky duck). I’m still doing a lot ‘wrong’ by keeping my NextEra utility stock for capital gains NUA and a whole bunch stuffed into the MM mattress. Both of these carry their own risk, but I am more comfortable with the present portfolio than the one in March. Very unnatural for me to have anything outside of equities after being all in for 32 years investing. Still, my risk tolerance has diminished as freedom approaches and have come to the realization that I don’t want the stomach churn of another tech bubble or financial crisis while going from accumulation to drawdown. Planning on getting a checkup from Fidelity FA soon – maybe he’ll help at this critical juncture.

Atom