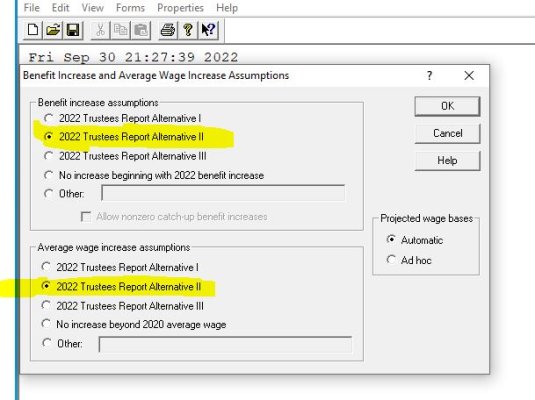

I was using the wrong indexing factors to manually calculate my wife and I PIA at age 67. To my surprise, I underestimated my wife yearly social security benefits by $3000 at age 62, and my yearly social security benefits by $8000 age 70.

Don't forget to use the future bend points in your calculation as well.

Is there a maximum Social Security retirement benefit payable? The amount at age 70 for me seems very high.

Below are 2 youtube videos that explains the calculation.

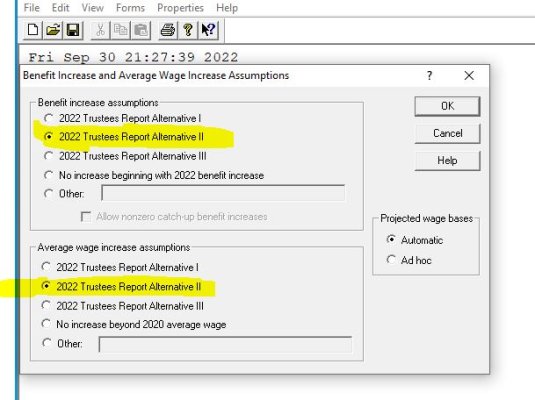

Don't forget to use the future bend points in your calculation as well.

Is there a maximum Social Security retirement benefit payable? The amount at age 70 for me seems very high.

Below are 2 youtube videos that explains the calculation.

Last edited: