As a CT resident I'd made up my mind to move to a low/no income state for retirement. So it was a surprise to find out recently that CT is becoming retirement tax friendly. Imagine that!

I've been crunching the "tax" numbers and they make retirement in CT look much more attractive such that I may just retire here and start my ROTH conversions.

In 2019 CT introduced new thresholds so there is no state income tax on social security payments with a 100% exemption if federal AGI is below $75k for singles and $100k for joint filers. If AGI is above $100k/$75k then its a 75% exemption.

Next they have introduced tax exemption for pension (401k, tIRA)and annuity income that is recorded on line 5b of your federal 1040.

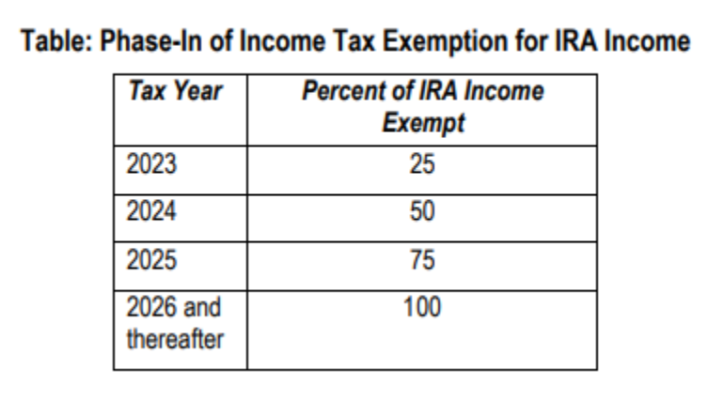

The exemption ramps in over 5 years (see the table below) impacts pension and annuity income for singles and joint filers with adjusted gross income (AGI) levels of up to $75k and $100k respectively.

TAX YEAR % EXEMPTION

2019 14%

2020 28% LAST YEAR

2021 42%

2022 56%

2023 84%

2024 100%

I've been crunching the "tax" numbers and they make retirement in CT look much more attractive such that I may just retire here and start my ROTH conversions.

In 2019 CT introduced new thresholds so there is no state income tax on social security payments with a 100% exemption if federal AGI is below $75k for singles and $100k for joint filers. If AGI is above $100k/$75k then its a 75% exemption.

Next they have introduced tax exemption for pension (401k, tIRA)and annuity income that is recorded on line 5b of your federal 1040.

The exemption ramps in over 5 years (see the table below) impacts pension and annuity income for singles and joint filers with adjusted gross income (AGI) levels of up to $75k and $100k respectively.

TAX YEAR % EXEMPTION

2019 14%

2020 28% LAST YEAR

2021 42%

2022 56%

2023 84%

2024 100%

Last edited: