retire@40

Thinks s/he gets paid by the post

- Joined

- Feb 16, 2004

- Messages

- 2,670

..

buy and hold

buy and hold

buy and hold...

Actually, that's been my overall strategy for the past couple of decades.

It's worked pretty well over the long term.

..

buy and hold

buy and hold

buy and hold...

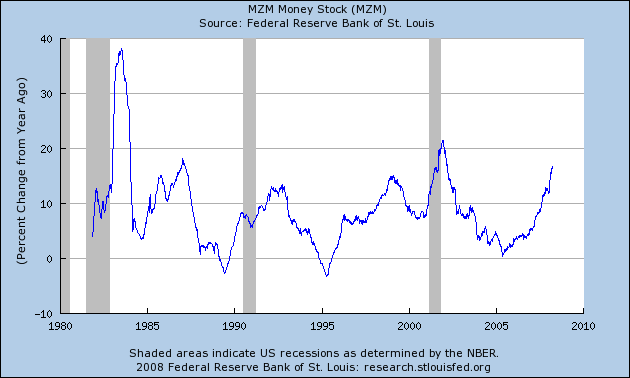

We're certainly in deflation already. Housing is deflating rapidly, 15% so far nationally, this will probably bottom out at 40% nationally unless it overshoots, I think the number is to the tune of a few trillion so far. All the bank writeoffs, over 500B so far, which will go to 1T, possibly as high as 2T - that's very serious deflation. The stock market is deflating, something like 2T so far. What else, I've heard that bonds, excepting the highest quality Treasury/Agency bonds, are suffering the same, but I haven't verified that. You can look at the various monetary indicators (MZM and the like), and velocity to see what's happening to money, it's slowing down and deflating.

.

Some ideas (from whichever source) are crummy that may lead one to lose a fortune.Lots of people will lose lots of money because some ideas are more equal than others?

What in the world does that mean?

")

There are two forms of deflation, 'asset deflation' that you point out and goods and services deflation that happened in the 1930's. Anyone who has hired a plumber and gone out to eat recently can tell you we don't have the latter.

That being said I would suspect that uncontrolled asset deflation would eventually cause goods and services deflation.

The sources of deflation are not a mystery. Deflation is in almost all cases a side effect of a collapse of aggregate demand--a drop in spending so severe that producers must cut prices on an ongoing basis in order to find buyers.1 Likewise, the economic effects of a deflationary episode, for the most part, are similar to those of any other sharp decline in aggregate spending--namely, recession, rising unemployment, and financial stress.

However, a deflationary recession may differ in one respect from "normal" recessions in which the inflation rate is at least modestly positive: Deflation of sufficient magnitude may result in the nominal interest rate declining to zero or very close to zero.2 Once the nominal interest rate is at zero, no further downward adjustment in the rate can occur, since lenders generally will not accept a negative nominal interest rate when it is possible instead to hold cash. At this point, the nominal interest rate is said to have hit the "zero bound."

Deflation great enough to bring the nominal interest rate close to zero poses special problems for the economy and for policy. First, when the nominal interest rate has been reduced to zero, the real interest rate paid by borrowers equals the expected rate of deflation, however large that may be.3 To take what might seem like an extreme example (though in fact it occurred in the United States in the early 1930s), suppose that deflation is proceeding at a clip of 10 percent per year. Then someone who borrows for a year at a nominal interest rate of zero actually faces a 10 percent real cost of funds, as the loan must be repaid in dollars whose purchasing power is 10 percent greater than that of the dollars borrowed originally. In a period of sufficiently severe deflation, the real cost of borrowing becomes prohibitive. Capital investment, purchases of new homes, and other types of spending decline accordingly, worsening the economic downturn.

Producer Price Index News Release text

Augusts PPI report is out.

Year over year percentage increase for finished goods was 9.6% in August.

Almost a 10% increase in finished goods from Aug 2007 to August 2008. Inflation is still alive, just hidden in government reports. Monthly variances and recent declines do take the PPI down a bit but otherwise there would be a panic on inflation.

When the government uses core inflation numbers things look very tame indeed and people start talking about deflation. But consumers don't just buy core products. That's the kick.

several on this board do their best to squash any reasonable discussion, and that's no fun

We're certainly experiencing deflation already

15% so far nationally

this will probably bottom out at 40% nationally

All the bank writeoffs, over 500B so far, which will go to 1T, possibly as high as 2T - that's very serious deflation. The stock market is deflating, something like 2T so far. What else, I've heard that bonds, excepting the highest quality Treasury/Agency bonds, are suffering the same

but I haven't verified that

You can look at the various monetary indicators (MZM and the like), and velocity to see what's happening to money, it's slowing down and deflating.

Simply, the last 25 years of leveraging up is now in the process of painfully deleveraging, which is deflationary.

At any rate, two years later, stocks are back where they were, and my bonds have returned maybe 20%

Compared to the house and stocks I sold to buy the bonds, I'm up about 50%.

Stocks are probably OK when IN deflation, but on the way to deflation they're not so good to own, which I think we've been seeing already.

That's good.........HOW would you be investing WITHOUT the pension??

Very true - but any ER/FIRE's biggest expenses are

And both of those are getting cheaper by the day, if you're positioned for it. Compared to that, the cost of eating out is nothing (and I don't even eat out

- Investments (1M+)

- House (several hundred thousand)

General price deflation/CPI is a distinct possibility I suspect - but who knows. My point is that if you become deflation aware, you can find lucrative investment possibilities that didn't seem possible before. Simply dismissing deflation out of hand makes you miss these opportunities.

I'm amazed that anyone is worried at all about deflation. I really don't think serious deflation is possible once you are off the gold standard, since it is the easiest thing in the world for the government to fix.

Too much deflation? Just print more money. Problem solved.

Does anyone really think that the government is going to keep money tight enough to actually cause deflation?

Just about everything around is more expensive than it was five years ago. A popping asset bubble is not really deflation, except over a very short timeframe.

Deflation is catastrophic to any government. They depend on inflating tax revenues. A dose of deflation will cause panic at any government entity. Just think what the impact of lower property tax assessments will mean. They are in a total panic.

The money belongs to the gov't. They print it, they let us hold it, then they take it back.

The money belongs to the gov't. They print it, they let us hold it, then they take it back.Did your corporate job's 401k or whatever not offer you a NON-equity investment option while you were still employed, or did you choose to be in equities then?

Actually, that's been my overall strategy for the past couple of decades.

It's worked pretty well over the long term.

Really ?

Have you cashed out your chips... or are you still letting them ride ?

~

Deflation is catastrophic to any government. ...

Just think what the impact of lower property tax assessments will mean. They are in a total panic.

If you lived in Texas I'd say you were full of sh*t. When property values go up, the pols are beside themselves to tell you the tax rate isn't going up even though you are paying more. They then tell you how every highshool "needs" their own natatorium and new uniforms for every team down to the chess club. If property values drop then you should be happy to have your tax rate go up "for the children."Lower property assessments would have zero impact in my local taxing district. They take the total of the assessments, then factor the tax by that.

If every home doubled in value, my tax bill would be the same. If every home value dropped in half, my tax bill would be the same. I think most communities work this way, but I don't know for sure. Based on the comments from some of my neighbors, I suspect that a lot of people don't know how their property taxes are structured.

-ERD50