brewer12345

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Mar 6, 2003

- Messages

- 18,085

A couple of our friends are having their rented outer boro of NYC digs sold out from under them. Since they are thinking about having kids, they have decided to look for a house. They looked in Westchester, but were appalled at the prices even after reductions. They were interested in NJ, so DW, some other local friends and I took them on a tour yesterday. I did most of the pseudo-realtor duties, including walking into several open houses as we were cruising around looking at neightborhoods. This was all in central NJ, mostly in Monmouth County. A few observations:

- There is a ton of stuff sitting on the market. 6 months, 9 months not uncommon, and we saw a number of properties that had seen asking prices reduced more than once (with clear intimations that asking prices were just that).

- Some of the 'hoods we looked at were original Levit developments, where the houses were pretty much the same in the same 4 basic models. Prices for the same model varied a bit by age and location, but the price range wasn't that wide and there appears to be a leapfrog effect where vcompeting properties keep chopping prices to get below the other guy.

- Why in Gawd's name would you try to sell a property with the original 60s asbestos shingles, even if they were still in good shape?

- Realtors are looking pretty sad and desparate, and a few even started to size me up as competition as I lead our friends into open houses. I thought this was curious since I was walking around in a faded t shirt, well worn costco shorts, and 3 days beard growth (practicing for ER).

- Even stuff with unique features or location seemed to be open to offers. We saw a ranch that had been turned into a mother-daughter (complete with second kitchen) and had the garage converted to a very nice den that was open to offers. Also saw the most immaculate 35 YO house I have ever seen on a really nice piece of property in a nice 'hood that had had the price slashed twice.

- We looked at a bank-owned property through the windows and stomped around the yard gawking. Really nice spot, but it needs a ton of work. No way they will get anything like their asking price. Even if they got their asking price, I would estimate that the bank will take a ~50% loss.

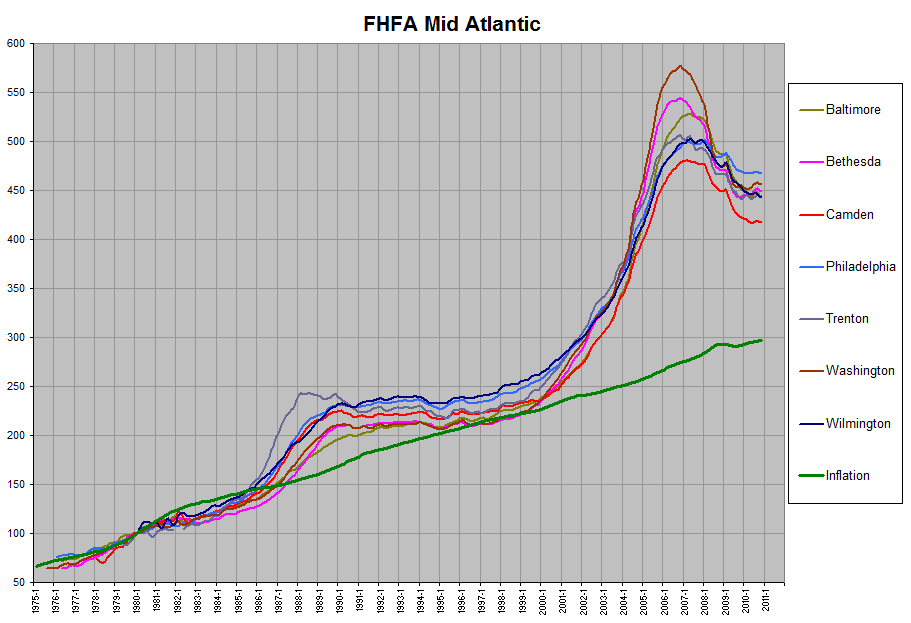

I think RE has a long way to go (down).

- There is a ton of stuff sitting on the market. 6 months, 9 months not uncommon, and we saw a number of properties that had seen asking prices reduced more than once (with clear intimations that asking prices were just that).

- Some of the 'hoods we looked at were original Levit developments, where the houses were pretty much the same in the same 4 basic models. Prices for the same model varied a bit by age and location, but the price range wasn't that wide and there appears to be a leapfrog effect where vcompeting properties keep chopping prices to get below the other guy.

- Why in Gawd's name would you try to sell a property with the original 60s asbestos shingles, even if they were still in good shape?

- Realtors are looking pretty sad and desparate, and a few even started to size me up as competition as I lead our friends into open houses. I thought this was curious since I was walking around in a faded t shirt, well worn costco shorts, and 3 days beard growth (practicing for ER).

- Even stuff with unique features or location seemed to be open to offers. We saw a ranch that had been turned into a mother-daughter (complete with second kitchen) and had the garage converted to a very nice den that was open to offers. Also saw the most immaculate 35 YO house I have ever seen on a really nice piece of property in a nice 'hood that had had the price slashed twice.

- We looked at a bank-owned property through the windows and stomped around the yard gawking. Really nice spot, but it needs a ton of work. No way they will get anything like their asking price. Even if they got their asking price, I would estimate that the bank will take a ~50% loss.

I think RE has a long way to go (down).