Graybeard

Full time employment: Posting here.

- Joined

- Aug 7, 2018

- Messages

- 597

Another very interesting and informative thread.

Not my style..Market conditions change over time and so should I..Doing nothing is too easy and that has cost me way more than taking action and making moves..For example I knew a year ago I should have moved out of my investment grade bond fund..Having served me well for 15 years it was easy to do nothing...BIG MISTAKE

And 28% in equities produces almost as much return as 60% in equities.

Which I think shows the power and value of equities.

But if you compound it over 30 years, that "almost as much" becomes a much bigger gap.

But if you compound it over 30 years, that "almost as much" becomes a much bigger gap.

But do you need the “extra” for a successful retirement? Take only as much risk as needed.

Not my style..Market conditions change over time and so should I..Doing nothing is too easy and that has cost me way more than taking action and making moves..For example I knew a year ago I should have moved out of my investment grade bond fund..Having served me well for 15 years it was easy to do nothing...BIG MISTAKE

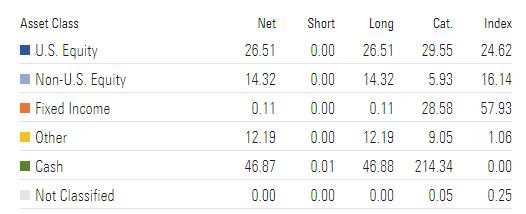

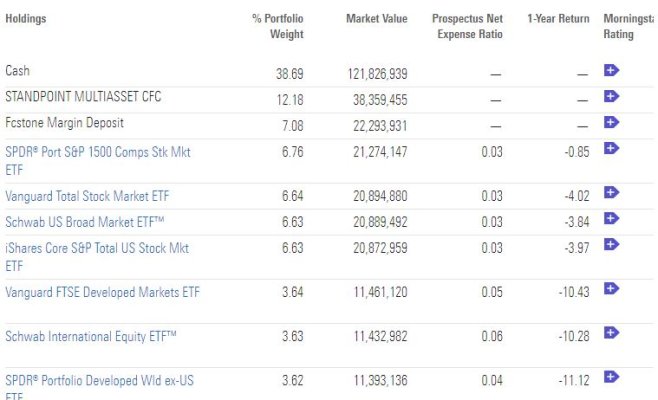

I was interested in the fund BLNDX and took a look. https://www.morningstar.com/funds/xnas/blndx/portfolioGood point.. The old risk/reward conundrum. In the end I'm one of those who do not have much tolerance for risk. At this point in my life I've decided I really do not want more in the stock market than I can afford to lose..That probably is not the best move statistically but I just don't have the stomach for it..

So you must have substantial percentage invested in other fixed income to average out to 20/80 overall as you mentioned early.

BTW, we are approx 50/45/5 equity/fixed/cash.

Anyone here have an opinion on BLNDX or other possibilities?

@lawman, there is nothing easier than market timing by looking in the rear view mirror. We have all been there: shoulda, coulda, woulda ...Not my style..Market conditions change over time and so should I..Doing nothing is too easy and that has cost me way more than taking action and making moves..For example I knew a year ago I should have moved out of my investment grade bond fund..Having served me well for 15 years it was easy to do nothing...BIG MISTAKE

I'm old and I can't afford another lost decade. Just sold half of my equity positions. Looking at a graph of the last 10 years I realized that I've done well enough. I don't want to lose ground over the course of a decade. I can't see me ever buying more equities on any significant scale..Now I need to figure out what to do with the money. I'm looking for something with less risk than the stock market but more risk than C. D.'s or treasuries. I do have one fund (BLNDX) that has been very good but even though it has been pretty steady I still wonder how safe it is..It's an all weather fund that trades in equities, currencies, commodities, and bonds.. On it's face it looks to me to be very high risk but they market it as an all weather fund that one might use to replace a bond fund..Anyone here have an opinion on BLNDX or other possibilities?

Those market timing quotes are all like saying even Jerome Powell doesn't know what interest rates are going to do, despite the fact that he is head of The Fed, the group that sets the federal funds rates and is in charge of quantitative easing.

We don't always know so clearly a year in advance what the Fed is going to do, but this year they have said at the start they intended to fight inflation as a priority and would be raising interest rates 6 - 7 times. So far they have kept their promise. If they change it they will post it in their meeting minutes. Their May meeting minutes were along the lines of full steam ahead on the interest rate increases. The people who ditched the longer duration bond funds after the Fed's announcements earlier in the year have pretty easily avoided 10% losses so far this year.

From the May meeting minutes: "Fed minutes released Wednesday indicated that officials are prepared to move ahead with multiple 50 basis points interest rate increases...In addition, the Federal Open Market Committee said policy may have to move past “neutral” and into “restrictive” territory." https://www.cnbc.com/2022/05/25/fed-minutes-may-2022.html

Not my style..Market conditions change over time and so should I..Doing nothing is too easy and that has cost me way more than taking action and making moves..For example I knew a year ago I should have moved out of my investment grade bond fund..Having served me well for 15 years it was easy to do nothing...BIG MISTAKE

True, but for example if one is still staying at their AA and moving bond fund allocations to CD's/MYGA's, etc, then that would not be a direct market timing as opposed to just getting out of stock into cash.

True, but for example if one is still staying at their AA and moving bond fund allocations to CD's/MYGA's, etc, then that would not be a direct market timing as opposed to just getting out of stock into cash.

Sir John Templeton: “The four most expensive words in the English language are 'This time it’s different.' ” Maybe. Maybe not.Those market timing quotes are all like saying even Jerome Powell doesn't know what interest rates are going to do, despite the fact that he is head of The Fed, the group that sets the federal funds rates and is in charge of quantitative easing.

We don't always know so clearly a year in advance what the Fed is going to do, but this year they have said at the start they intended to fight inflation as a priority and would be raising interest rates 6 - 7 times. So far they have kept their promise. If they change it they will post it in their meeting minutes. Their May meeting minutes were along the lines of full steam ahead on the interest rate increases. The people who ditched the longer duration bond funds after the Fed's announcements earlier in the year have pretty easily avoided 10% losses so far this year.

From the May meeting minutes: "Fed minutes released Wednesday indicated that officials are prepared to move ahead with multiple 50 basis points interest rate increases...In addition, the Federal Open Market Committee said policy may have to move past “neutral” and into “restrictive” territory." https://www.cnbc.com/2022/05/25/fed-minutes-may-2022.html

Speaking of funds, after listening to some here talk about the advantage of individual bonds over bond mutual funds I have been looking at going the individual route with all the cash I have accumulated now and parked in 1- 6 month cd's and treasuries.. What I've found is I cannot find issues that I would be comfortable holding that pay anywhere near what my old fund is now paying (VFIDX). That fund has a distribution yield of 2.99% and and a SEC yield of 4.2%. I have tried to understand the difference between the two but I still cant understand how those numbers could be so far apart..I suppose once the Fed slows down on interest rate increases perhaps the fund might once again be prudent..