They can't be "accurate" as there are way too many variables they can't "know." Unless you can project longevity, market returns, inflation, future Soc Sec, geopolitical events and future tax rates - among other variables, no calculator can "predict" anything. The best they can do is tell you how you would have fared in the past (FIRECALC) or how you would fare based on whatever assumptions you/they are using. Many of the free calculators don't even disclose their assumptions.

And if the tool is wrong, you probably won't know it until it's too late, long after you've retired. You decide what safety factors you need to sleep at night, and take your chances...

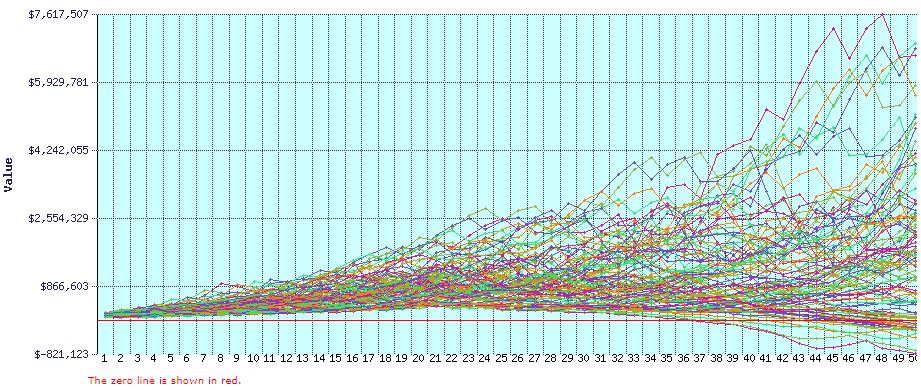

Look at the range of actual historical outcomes FIRECALC generates. Any reason to expect the future would be more predictable?