our plan includes some assumptions for some explicit declines in spending compared to today. My spreadsheet has 1) today's expense rate, 2) when we sell big home and move in a few years, 3) when the kids are out of college and indepdendent 4) when we are 70 and SS/Medicare/RMDs kick in (I know medicare kicks in before 70 but just used 70 to simplify.

Do you pro-forma model reduced expenses in the future or is that too risky?

Some of the bigger $ examples

- property taxes, mortgage, upkeep expenses on our big primary home which we will sell once the kids are all away @ college. Assuming smaller home expenses.

- reduced cost of health and auto insurance when kids are off our plans in mid 20's

- reduced groceries and other expenditures when no longer have three teen boys @ home

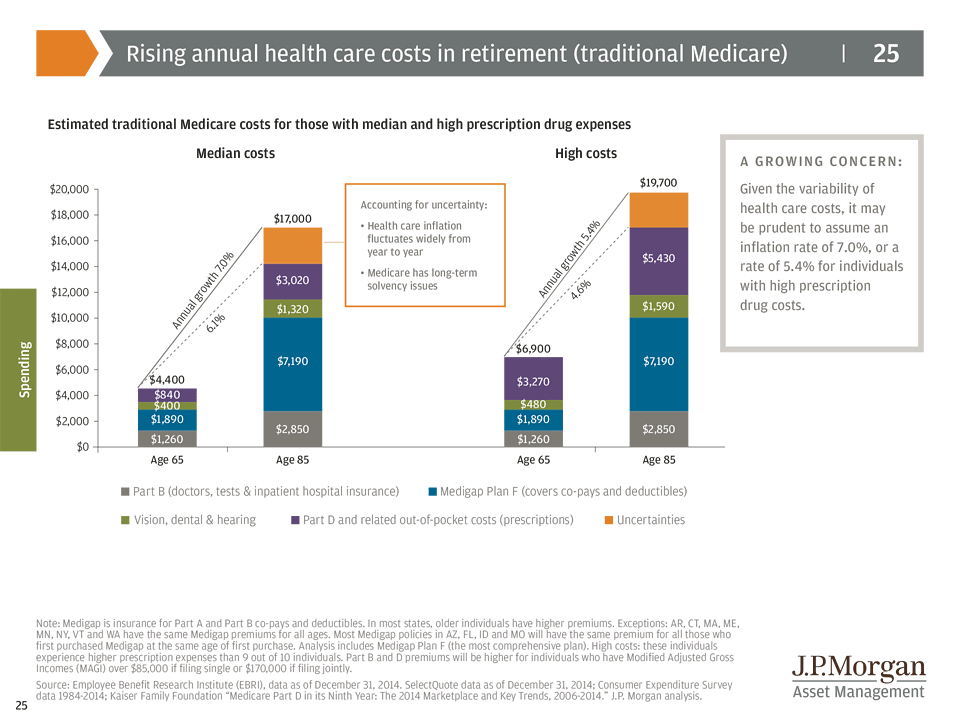

- medicare vs private health care

Do you pro-forma model reduced expenses in the future or is that too risky?

Some of the bigger $ examples

- property taxes, mortgage, upkeep expenses on our big primary home which we will sell once the kids are all away @ college. Assuming smaller home expenses.

- reduced cost of health and auto insurance when kids are off our plans in mid 20's

- reduced groceries and other expenditures when no longer have three teen boys @ home

- medicare vs private health care

. I recall it showed retirees just don't spend as much on most things as they get older, but late stage retirement medical care expenses begin to increase. What was reassuring to me was that although medical expenses rose in late retirement, it didn't surpass spending in early retirement, due to the offset of decreased discretionary spending. Again, I personally am not at all comfortable planning on any type of reduced spending, and intend for any actual reduced spending to act as a buffer/cushion.

. I recall it showed retirees just don't spend as much on most things as they get older, but late stage retirement medical care expenses begin to increase. What was reassuring to me was that although medical expenses rose in late retirement, it didn't surpass spending in early retirement, due to the offset of decreased discretionary spending. Again, I personally am not at all comfortable planning on any type of reduced spending, and intend for any actual reduced spending to act as a buffer/cushion.