mountainsoft

Thinks s/he gets paid by the post

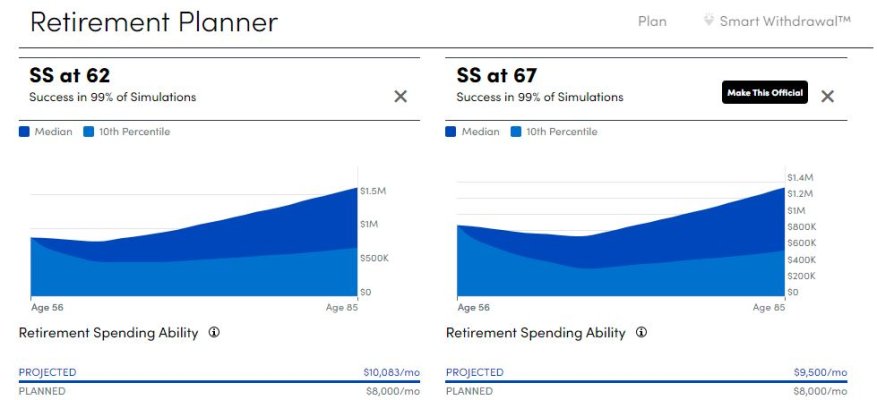

I retired at 55. Six years later I am approaching the point where 'when to take Social Security' (SS) becomes more than an academic question.

I have been modelling different scenarios around taking SS at 62, 65, 67 and 70 years of age.

How has any modelling you have done played out?

What I do is log on to "My Social Security" account and determine the amounts that would be paid at each age (62, 63, etc.). Then I multiply each of those values by 75% to account for the "haircut" if social security is not fixed before the trust fund runs out.

Next, I enter each value in "Flexible Retirement Planner" as a separate entry in the "additional inputs" section. I use a "track inflation" COLA and assume 85% of SS will be taxed.

I also enter all other values in FRP as usual, pensions, savings, other income sources, etc.

Once I have everything in FRP I can experiment by selecting different SS options for my wife and I. For example, if I start at 62 and she starts at 67. Or if we both start at 62, or both at 70.

I find there is a tradeoff. The longer we wait to take SS, the more of our personal retirement savings we'll spend down. It's a matter of balancing how low we want our savings to get before we start SS.

A couple years ago it looked like 62 was going to be the best time for both of us to start SS. As our retirement savings have grown over the last few years, we will probably be able to wait until 64 or 65. We still have a couple years before we retire, so we may end up pushing the SS start dates even further.

Basically, we will wait and see where we are when we get closer to starting SS. If we need the money, we'll take it. Otherwise, we'll postpone SS as long as possible.