MichealKnight

Full time employment: Posting here.

- Joined

- May 2, 2019

- Messages

- 520

Ladies, Gents, Conservatives, Liberals, Vegetarians, Libertarians and all the ships at sea........

I'm going to ask this crystal ball question, but preface it with a few pleas:

*FireCALC: Yes, aware of it, have played with it.

*Market Timing - fully agree, not always possible.

So hoping for actual guesses....or basic opinions - free of our feelings on market timing or our devotion to firecalc.

Really hoping for people's opinions...no different than picking a stock, or making a sports prediction.

For a 7-10 year outlook..... and a 60/40 portfolio.... what do you feel is a realistic years return. NOMINAL return.

The reason I ask... if I early retire in 2020.... the nominal returns I'm hoping for hover around 5.25%-5.5%.

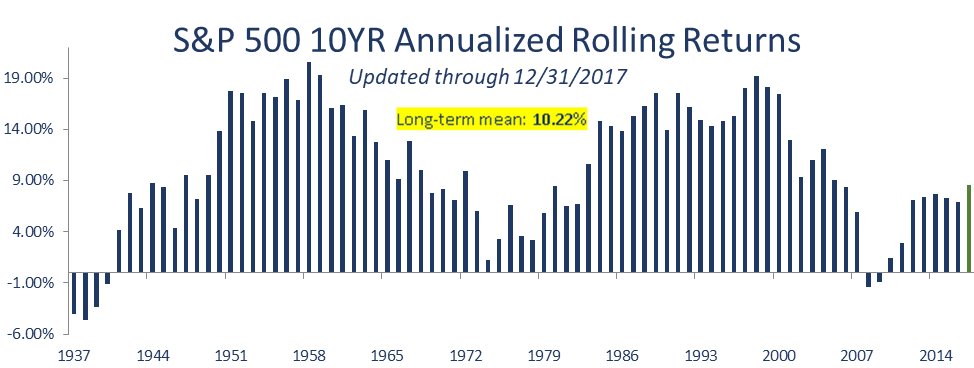

I look at the popular VWINX (Wellesley)....and of course the last 40+ years shows a nice 9% return. Many states seem to depend on 8% returns for their pensions. So when I see those numbers, I feel that my 5.5% desire is almost 40% LESS than people are used to in recent decades. Frankly I wonder what a 40% drop in investment income would mean for the nation and world but I digress.

Bottom line: is 5.5% (NOMINAL). wishful pie in sky thinking? Is it a slam dunk? Is it sort of realistic? Would really appreciate your guesses or opinions on this...and specifically, what you feel a 60/40 portfolio might return over the next 7-10 years.

Thanks for reading.

I'm going to ask this crystal ball question, but preface it with a few pleas:

*FireCALC: Yes, aware of it, have played with it.

*Market Timing - fully agree, not always possible.

So hoping for actual guesses....or basic opinions - free of our feelings on market timing or our devotion to firecalc.

Really hoping for people's opinions...no different than picking a stock, or making a sports prediction.

For a 7-10 year outlook..... and a 60/40 portfolio.... what do you feel is a realistic years return. NOMINAL return.

The reason I ask... if I early retire in 2020.... the nominal returns I'm hoping for hover around 5.25%-5.5%.

I look at the popular VWINX (Wellesley)....and of course the last 40+ years shows a nice 9% return. Many states seem to depend on 8% returns for their pensions. So when I see those numbers, I feel that my 5.5% desire is almost 40% LESS than people are used to in recent decades. Frankly I wonder what a 40% drop in investment income would mean for the nation and world but I digress.

Bottom line: is 5.5% (NOMINAL). wishful pie in sky thinking? Is it a slam dunk? Is it sort of realistic? Would really appreciate your guesses or opinions on this...and specifically, what you feel a 60/40 portfolio might return over the next 7-10 years.

Thanks for reading.