scrabbler1

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Nov 20, 2009

- Messages

- 6,699

Very nice. Congrats. Love it when we add commas

...and when we have to widen columns, too!

Very nice. Congrats. Love it when we add commas

was that directed at me?

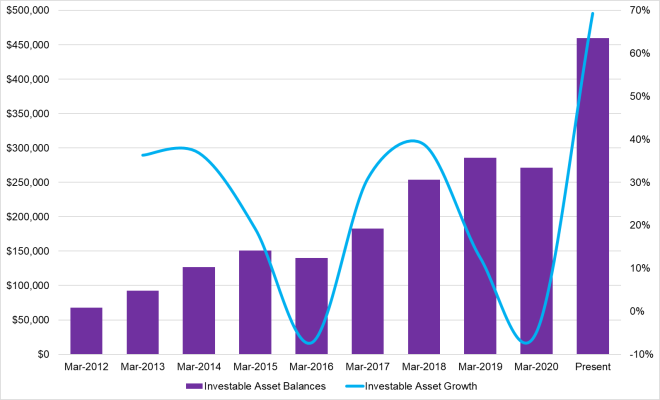

I charted my aggregate IA asset balances and growth % y/y for the last 9 years (that's how long I've been keeping detailed records). On average, 26% growth y/y - not too shabby! But when you remove the best performing year @ 69% growth (Mar-2020 - Mar-2021) -aka- "The Year of COVID" - the average drops to 20%. Anyone else track like this that is willing to share? I found it insightful.

I do. We averaged 28% annual y/y past 8 years since I started tracking.

That’s all in for me.ATXFIRE and kgtest, do those percentages include yearly contributions as well or just market returns?

Dash man that is awesome and it doesn't happen by accident!!! Is that NW or just portfolio??

Not sure I will ever make that milestone but I'm well over half way there now (NW) and over half in portfolio also.

Regardless of what we have in NW, I feel so blessed to have my health and things I love so much.

Ohhhhh Nooooo don't feel that way. We all can work longer and keep making milestone come faster but that isn't what we should do. I hope you retire when you feel ready regardless of the amount.You guys make me unretireable. I could reach 8 figures if I wanted to work to my 70 years. I don't even want to work to my 60s, but I do like more money.

This is a very good achievement.At the end of March my trailing 12mo expenses hit 2% of my liquid net worth (excluding taxes) for the first time.

This is a very good achievement.

I just calculated my number and it is 2.8%. Do we have a magic number to reach for ER?

You guys make me unretireable. I could reach 8 figures if I wanted to work to my 70 years. I don't even want to work to my 60s, but I do like more money.

^ interesting correlation.

My yearly expenses are .7% of liquid portfolio. My WR is less then .7% every year so far in retirement, except last year. Charity and gifting made that number rise to ~2%.

Another year and half passed. Time to update my stats:

After tax account: 1.8

Retirement account: 5.6

Rental Property: 4.4

Primary Residence 3.0 -0.8

total: 14.0m

Big bump from last update thx to the rising stock and housing market.

I joined this forum 7+ years ago, saying I plan to fire in 7 years when

my kid gets out of college.

I guess I get OMY syndrome. A few more years, but 5 more years at most when I pay off my house

Another year and half passed. Time to update my stats:

After tax account: 1.8

Retirement account: 5.6

Rental Property: 4.4

Primary Residence 3.0 -0.8

total: 14.0m

Big bump from last update thx to the rising stock and housing market.

I joined this forum 7+ years ago, saying I plan to fire in 7 years when

my kid gets out of college.

I guess I get OMY syndrome. A few more years, but 5 more years at most when I pay off my house