Sunset

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

TD Bank calls off merger with First Horizon. This is good news for TD Bank as they were overpaying based on a price set early last year. TD Bank shareholders were urging the bank to terminate the deal after the deposit flight at First Horizon.

https://www.wsj.com/articles/toront...inate-merger-agreement-38d58b35?siteid=yhoof2

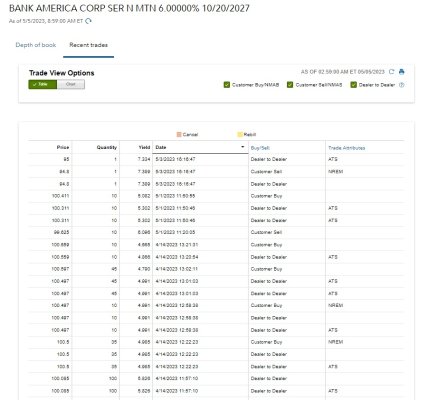

Now that they don't need so much cash, I wonder if they will call some of their bonds paying over 5.5% ?