kcowan

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Did not include house. Did include cash and bonds.

5.37% YTD down from 10.59% YTD May

Last year 10.95%

5.37% YTD down from 10.59% YTD May

Last year 10.95%

")

ladelfina said:sorry Spanky.. I was confused too, and looked at your figures without realizing they made no sense with your bottom line..

retire@40.. uhmmm.. do you account for all your repair expenses in that figure? Do you count opportunity value of home equity vs. a MMF? Or do you use a monthly rental value for similar property as an inherent "dividend"?? Since people usually buy the homes they do for reasons other than the concrete investment growth/income that they get from stocks/bonds.. I'm not sure that it's a reasonable comparison in this context (performance vs. the market). If it's just for personal enlightenment, by all means, knock yourself out!

MyDream.. as you can see we DON't always know what one another is talking about! (but we try..). The original question was phrased in a bad way and asked for a number few people would bother to compute if they had to do it by hand: what percentage over your initial investments have you gained from a certain date (1/1/05) until now (10/17/06); most people, when and if they look at such a number, tend to think of it on a calendar year basis.

If I start on 1/1/05 with $100k and end on 12/31/05 with $108k, then my Total Return is 8% for the year. The trick is to make sure that any dividends, withdrawals, re-investments, etc. are duly accounted for. If your stock/fund/bond/whatever market value is $108k on New Year's Eve, but you have received $2k of interest or dividends over the course of the year and these have gone to your cash account, then your Total Return for that holding is not 8%, but 10%. Does that make sense?

Just take it one step at a time and you'll get there.. I know sometimes it seems like drinking from the proverbial fire hydrant... (for me, too).

My Dream said:After reading this post again, I need to go get some aspirins and lay down. This is so fricken confusing, and I'm so jealous that you all understand what the heck you're talking about. My compliment to you saps.

REWahoo! said:A handful of low expense mutual funds and a comfortable mattress are all I need to sleep soundly every night.

)My Dream said:Does the 4% rule assume that you will be withdrawing 4% from you're investments each year and if you do average let's say 10% each year, you leave the 6% in each year to allow for inflation and just let your pile grow?

Well, that's why we have to do it so often.LOL! said:Even with measuring with genetalia size there are problems.

This poll and many of the comments are a good example of overcomplification.My Dream said:After reading this post again, I need to go get some aspirins and lay down. This is so fricken confusing, and I'm so jealous that you all understand what the heck you're talking about. My compliment to you saps.

Yes.My Dream said:Forgive me for highjacking this thread, but if I may ask a question?

Does the 4% rule assume that you will be withdrawing 4% from you're investments each year and if you do average let's say 10% each year, you leave the 6% in each year to allow for inflation and just let your pile grow?

My Dream said:Forgive me for highjacking this thread, but if I may ask a question?

Does the 4% rule assume that you will be withdrawing 4% from you're investments each year and if you do average let's say 10% each year, you leave the 6% in each year to allow for inflation and just let your pile grow?

REWahoo! said:Yes, because your investment returns will fluctuate and you will have negative growth in some years. Since you want to continue to withdraw 4% anually (inflation adjusted), you will need to "bank" the good years or face the possibility of exhausting your portfolio and living on cat food.

Those taxes better come out of that 4%, otherwise your real withdrawal rate is quite a bit higher than 4% and your portfolio won't have as good chance to survive.Nords said:And remember that we have to take out enough from that portfolio to pay our taxes, too...

ladelfina said:...do you account for all your repair expenses in that figure? Do you count opportunity value of home equity vs. a MMF? Or do you use a monthly rental value for similar property as an inherent "dividend"?? Since people usually buy the homes they do for reasons other than the concrete investment growth/income that they get from stocks/bonds.. I'm not sure that it's a reasonable comparison in this context (performance vs. the market). If it's just for personal enlightenment, by all means, knock yourself out!...

Hey- conga rats - I even looked at you latest posts to see if I misssed an official notice.CyclingInvestor said:Time horizon : age 48, retirement date Oct 17,2006

sailor said:Hey- conga rats - I even looked at you latest posts to see if I misssed an official notice.

So, what do you do whole day?

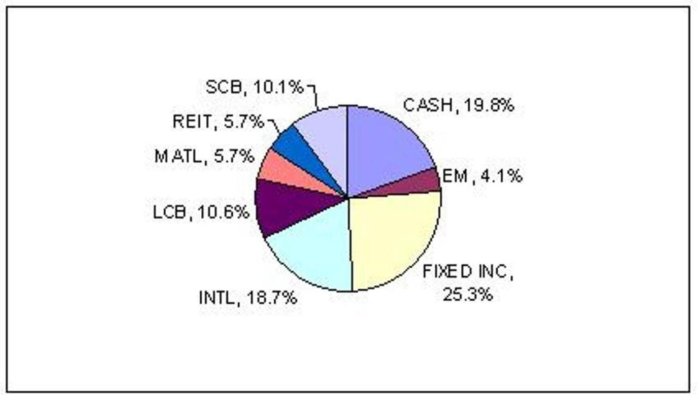

modhatter said:Spanky: You have done well also in a 60/40 split, and only one to give asked breakdown. You sure had faith in the international market. (24.72%) Good for you. Takes some courage. Do you do mostly individual stocks, indexes or managed funds?

You're welcome, but check your PMs for the rest of the story...My Dream said:Thanks REWahoo!, Nords and donheff , I appreciate the explanation.