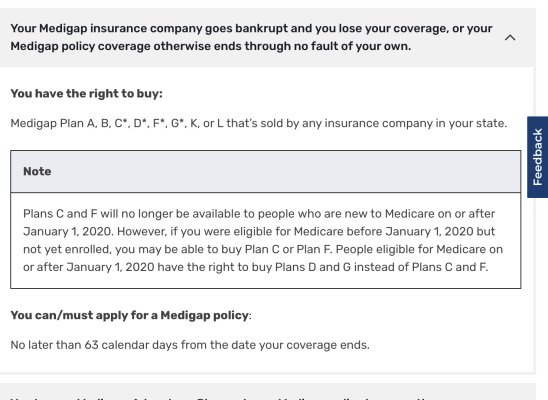

Bad thought I just had. Guaranteed Issue Rights.

Current plan F-HD.

If current insurance company decides to end the plan/get out of business.

You can get the same supplement without underwritting,from a different company. This has happened twice to me so far.

So what happens if that plan is not offered anymore in your state,and

you can't pass underwritting. If you entered medicare before 01/1/2020

you can't get plan G without underwritting.

Seems like this could be a real problem,say x number of years from now

and no one is offering plan F. Or will plan F will always have to be offered.

Oldmike

Current plan F-HD.

If current insurance company decides to end the plan/get out of business.

You can get the same supplement without underwritting,from a different company. This has happened twice to me so far.

So what happens if that plan is not offered anymore in your state,and

you can't pass underwritting. If you entered medicare before 01/1/2020

you can't get plan G without underwritting.

Seems like this could be a real problem,say x number of years from now

and no one is offering plan F. Or will plan F will always have to be offered.

Oldmike

Last edited by a moderator: